Why We Need to Repeal ALL Property Tax:

Talking Points & Letters to Write

By Mitchell Vexler, February 21, 2026

Why we need to repeal ALL property tax:

1. Violation of 16th Amendment

- People are taxed out of their homes, adversely impacting senior citizens with homes paid off.

- Financially bankrupting Homeowners forcing them to sell their home and move.

- Young Adults are priced out of Home Ownership. Appraisal District software helps set fraudulent floor on home prices.

- You will never own or have the opportunity to own the roof over your head.

- Equity stolen. The real estate tax steals what would be your amortized equity and that is equity stripping.

- Your real estate tax is their mechanism to fund fraudulent ISD Bonds and pay for the interest on those fraudulent bonds for as long as those fraudulent bonds exist.

- The majority of school districts that raise bond money are bankrupt and property tax payers are paying to delay their eventual bankruptcy. It is literally shoving hard earned money into the pockets of lenders who invested in fraud.

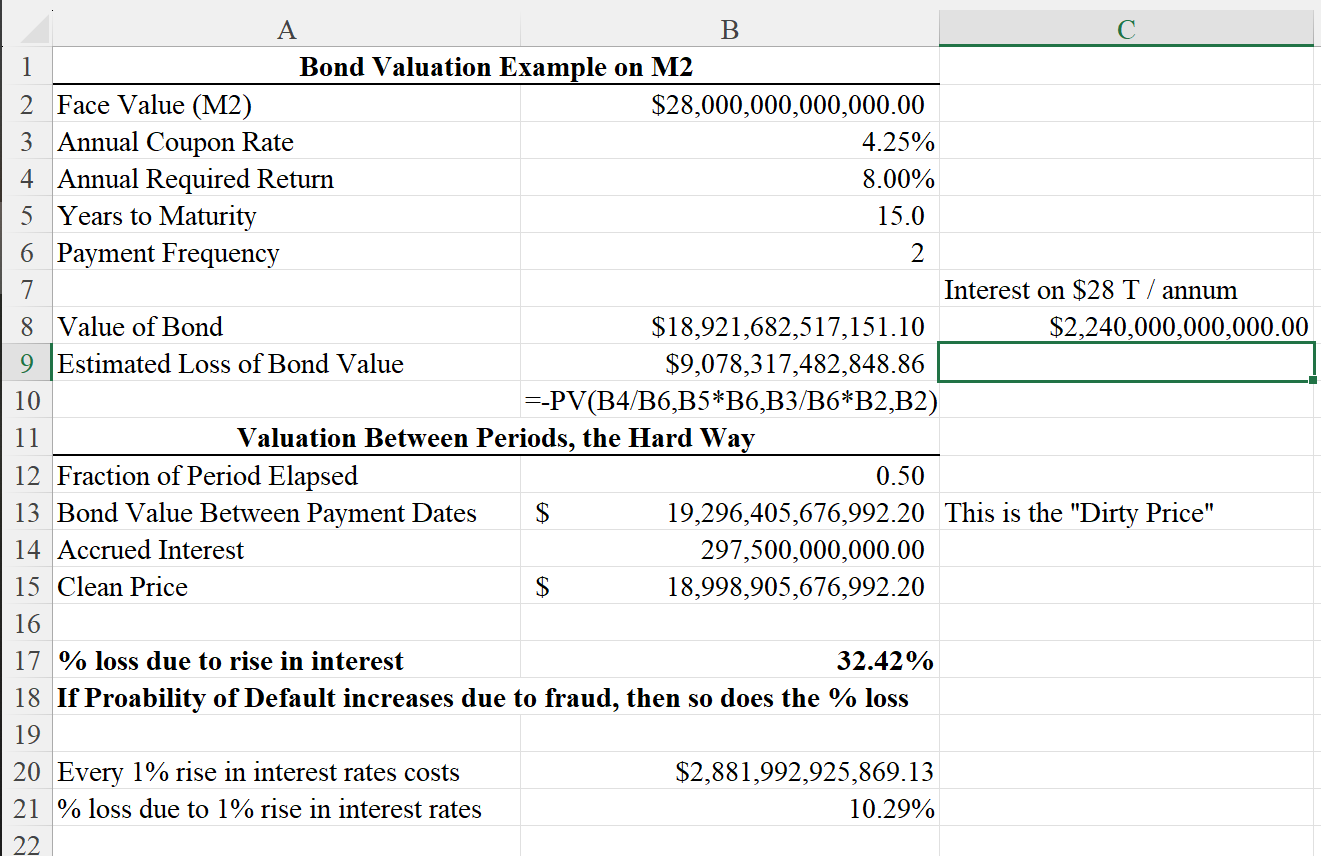

2. 2008 bank crisis + this bond crisis = many times worse than Enron

See Amicus Brief filed with the Supreme Court of Texas.

Example: May 2025, Celina ISD (Independent School District) was recently able to pass $2,275,695,579 in bonds. There are approx. 9,377 households in Celina, TX. That’s $242,689 in ISD debt per household, in 1 year, without counting the servicing interest or the past bond raises or the off-balance sheet financing.

- Bonds do not pay teacher salaries or any M&O (Maintenance and Operations)

- Large amounts of ISD bonds are purchased through Teacher Pensions

- Large amounts of ISD bonds are purchased by institutions as a collateral requirement

- AAA Credit Ratings based on “Unlimited Ad Valorem Pledges” or “Unlimited Tax” (no such thing)

- Bond debt has skyrocketed and mathematically cannot be paid back as is required in law. The underwriting of the bonds cannot be backed up based on fundamental math.

- ISD Bonds are insolvent which has bankrupted cities and schools & property owners.

- The interest to service $2 billion in Bonds over 30 years is approximately $9 billion in additional cost not including new bonds.

- This issue is playing out not just in Texas but across the U.S.

3. There is No Recourse or Due Process. Property Rights stripped, violates 5th & 14th Amendment.

- CAD (Central Appraisal District) is responsible for accurately valuing our homes.

- ARB (Appraisal Review Board) is supposed to support property owners in protesting their home value when a property owner does not agree with the CAD’s home value.

- The CADs often use renegade value software that falls out of legal requirements in order to back the CAD’s pre-determined budget into a home value. This allows them to achieve higher revenue and has nothing to do with USPAP – Uniform Standards of Professional Appraisal Practice. See partial list of violations of law by the CADs and school districts.

- The CAD and the ARB are working together, often to bully and confuse homeowners into accepting an overvaluation.

- The CAD & School Districts claim immunity and use the Appraisal Review Board, as the exclusive remedy, which is a Constitutional issue because the ARB does not have the authority or ability in law to determine fraud thus the ARB itself is aiding and abetting fraud. In Federal law, there is no immunity for fraud.

- Protest process is not fair or uniform and equal as required under law and in the Texas Constitution.

- All past and future data has been intentionally corrupted by using software that allows the hand overwriting of values, meaning the software is designed to allow fraud to be committed.

SOLUTION: Bill to Repeal all Property Tax in Favor of the Uniform States Sales Tax (follow link)

- Immediately end all property tax in favor of the Uniform States Sales Tax

- In Texas, Sales Tax goes up to a maximum of 15% for 3 years until stabilization. There should be 0 (zero) bonds remaining after 3 years. And if they cannot be paid off in 3 years, the bonds and schools districts are put into bankruptcy and the liability removed from the back of all property owners, thus all property tax repealed. Then after year 3 years the Sales Tax drops to 11-12% moving forward because the fraud has been removed from the system.

- No impact on food and medicine except for potential deflation.

- STOPS all Bonds and requires ISD’s turn over all the accounting, including the bond CUSIP’s and amortizations schedules, within 60 days of passing the Bill to Repeal All Property Tax.

- Within 60 days ISDs must prove ability to pay off all Bonds within 3 years or face immediate Bankruptcy.

- Eliminates Billions in agencies’ waste fraud and abuse, thus reducing the revenues needed.

- Puts money back into the classrooms and promotes quality teachers and higher teacher pay.

- Requires transparency to the public, fully visible via transparent on-line check registers from the State Comptroller’s office.

- All property owners will own their land and thus restore the amortization schedule from which to build their equity rather than having that equity stripped via fraudulent real estate tax and fraudulent school district bonds.

Everyone needs to take action now:

To get started, write a FOIA Letter to your school district superintendent.

From:

[insert name, address, email, and phone number]

To:

[insert District Superintendent name, address, email]

[insert date]

Dear School District Superintendent, [name]:

Under the FOIA (Freedom of Information Act) please provide the following:

- A Bond Schedule stating all outstanding individual school district bonds, including term, interest rate, underwriter, purpose, conditions, and their corresponding CUSIP numbers from 9/1/2001 to 9/1/2026,

- The amount of cumulative interest, outstanding interest and or compound cumulative interest on the outstanding bonds as of 9/1/2026,

- The amount of interest to be paid in the future on the outstanding bonds starting 9/1/2025 to 9/1/2045,

- The name of the Auditor and Auditing / Accounting Company, address, phone number and email address, hired by the School District.

I look forward to receiving the above documents.

Respectfully submitted,

[signature]

Or you can visit your school district website and try to gather the information on outstanding bond debt.

If you can get to the truth of the current outstanding school district interest and the current outstanding bonds, then divide that figure by the number of houses in the school district and you have the severity of the truth.

With regard to property valuations for ad valorem taxation purposes, property taxes assessed, and the outstanding municipal & school district bonds, ask yourself these questions:

- What proof exists that the certified taxes are correct?

- What proof exists that on an individual or global basis the certified taxes are correct ?

- If not correct and used as a basis for a property tax and school district bonds, how do homeowners recover from that lack of authority?

- Where is their data?

- No one has met the requirement of proof.

- Where is the verification of evidence?

- Where is the verification that the process, as required in law, was adhered to?

- Why is that, in the ARB hearings, we cannot question the process by which the ARB, or the appraisal district, comes to a number. (ARB or Appraisal Review Board in Texas is same thing as Board of Equalization in CA) This is the Vexler case now in front of the Supreme Court of Texas.

Billions of dollars of fraud have been put on the property owners back, which if recognized as fraud, they are not required to pay.

Intentional, willing suspension of disbelief exists.

Nothing meets the standard of what is required – That is the BIG CON!

We have the data and it is on the website free for all to see and use… at www.mockingbirdproperties.com/dcad and in the Articles, Letters & Discussions section.

Another step would be to write a letter to your Mortgage Lender with regard to Mail Fraud and send a copy to the FDIC chairman.

From:

[insert name, address, email, and phone number]

To:

[insert Mortgage Lender Company president name, address, email]

Copy:

Mr. Travis Hill, Chairman of FDIC

Federal Deposit Insurance Corporation

Division of Finance

3501 North Fairfax Drive

Building E, 5th floor

Arlington, VA 22226

[Insert Date]

Dear [Mortgage Lender Company] president, [name]:

I respectfully submit this request for attention regarding systemic concerns of mail fraud being promoted by my mortgage lender where I receive a monthly mortgage statement which has been compiled with fraudulent school district bond financing and fraudulent property tax practices and which may implicate violation of federal securities laws in addition to mail fraud.

Background

Texas school district and charter district bonds are marketed nationwide to investors and are enhanced through the Texas Permanent School Fund Bond Guarantee Program.

According to the Texas State Auditor’s January 2024 certification (Report No. 24-011), the Program guaranteed $115.7 billion in outstanding bond principal as of August 31, 2023, and was within statutory limits.

While formally compliant, the Program masks a growing insolvency risk. The underlying property tax base is inflated by systemic over-valuation. In some counties, more than one-third of households face unsustainable tax burdens, with lien rates reaching 23%, even on debt-free homes. In Argyle, Texas, school bond obligations equal approximately $343,000 per household against a median home value of $450,000.

In Celina Texas, the situation is worse than Argyle. In Celina, the Total Current ISD Debt and Interest is $5,354,573,893, with each housing unit having approximately $328,058 in debt, and where its future population could never grow enough to pay off the bonds.

These problems are being see across the United States and not just in Texas.

Concerns

- Potential Securities Misrepresentation

- Official Statements and bond offering documents describe repayment sources as “unlimited tax” obligations. In practice, median household incomes cannot support repayment of principal and compound interest, raising the risk that “unlimited tax” language misleads investors in violation of Exchange Act Rule 10b-5.

- Systemic Risk Beyond Texas

- The analysis filed in Vexler v. Denton Central Appraisal District (Supreme Court of Texas) demonstrates that these practices are not isolated. The financial exposure resembles Enron-style off-balance-sheet structures, but on a larger scale, affecting public finance nationally.

- Constitutional and Procedural Limits

- Lower courts acknowledged evidence of fraud but held that review ends at appraisal review boards (ARBs). The Texas Supreme Court’s precedent in Patel confirms that administrative bodies cannot insulate constitutional or fraud claims from judicial review.

I respectfully request that my mortgage lender from which I receive monthly mortgage statements immediately:

- Open a formal investigation into whether Texas school district bond disclosures misrepresent repayment security, thereby violating federal anti-fraud provisions.

- Utilize their authority to obtain documents withheld by the Texas Attorney General’s office that were previously sought under FOIA and relevant state public-records requests.

- Consider intervention by filing a statement of interest or similar action to ensure that federal securities law considerations are presented to the Supreme Court of Texas in Vexler v. DCAD.

Public Interest

This case has drawn significant public attention, with recent public briefings receiving more than 350,000 direct views and over 6 million aggregated impressions. These numbers reflect widespread concern over property tax insolvency and its impact on both homeowners and municipal bondholders nationwide.

Issue

Given the amount of overpayment on my mortgage via the fraud which I have calculated at $[insert amount], I am hereby making demand for the return of that overpayment. [Insert the amount of taxes assessed and paid to date due to the over-valuation of your property.]

Conclusion

You, as the mortgage lender, have a critical role in ensuring accuracy and integrity of your mailed mortgage statements as well as integrity of the municipal bond markets.

While Texas’s Permanent School Fund Guarantee Program may appear compliant under statutory caps, the disconnect between “unlimited tax” pledges and actual repayment capacity raises serious investor-protection concerns under federal securities law as does the mailing of statements which are comprised of fraud thus making those statements mail fraud.

I look forward to your immediate response.

Respectfully submitted,

[signature]