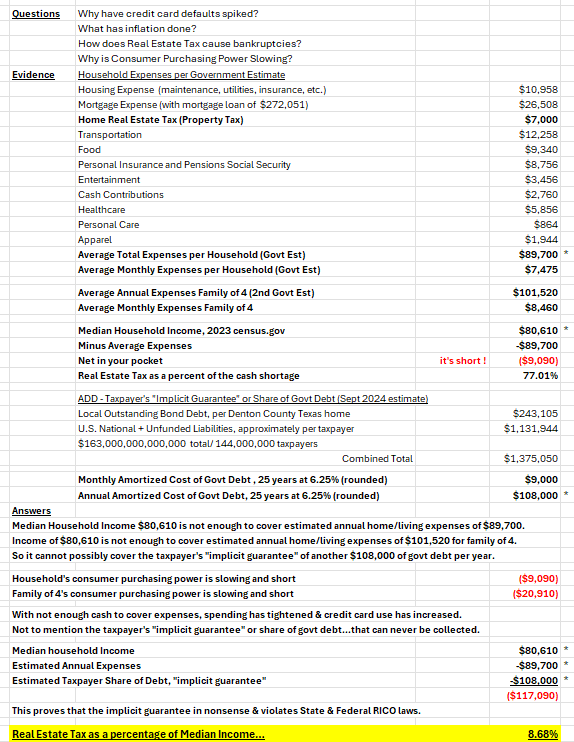

Systemic Institutionalized Moral Hazard:

School Districts and Central Appraisal Districts

By Mitchell Vexler, October 25, 2025

Current Status 10/25/25:

All property owners and taxpayers bear the responsibility to ensure that the School Districts and Central Appraisal Districts are adhering to the law.

The law is to be applied with accuracy and fairness.

The mission is fairness, not being the victims of bureaucracies.

For reasons of posterity we are documenting the history of the evidence to ideally ensure that such malice, arbitrary and capricious, financial crimes against humanity, with the backstop of the court system being sovereign immunity with no accountability, never happens again. In order to move forward, one must understand history so as not to repeat it.

The issues raised herein, are not just applicable to Denton Central Appraisal District, but are applicable across Texas and the United States.

There is a beginning, middle and end. To this point the beginning is the history which can be seen in the evidence and details presented at www.mockingbirdproperties.com/dcad and via the petition below. The middle is the process and means to achieve the end. Your involvement is needed to help through the process to make history and repeal all property taxes in favor of the Uniform States Sale Tax.

Let’s examine what is necessary to turn the tide toward the end. The following Petition is the summary of a massive amount of time, money and effort to distill the case down to its constitutional foundation.

The key phrase in the below Petition for Review is “If left undisturbed, the decision below would permit executive branch agencies to implement systematic constitutional violations immune from judicial review, so long as the Legislature has created an administrative process—however inadequate—to address individual disputes. This places executive action beyond constitutional scrutiny and requires this Court's correction.

In other words, if not addressed, the courts have created no law for the protection of the property owners.

Here are excerpts from the Petition for Review:

II. ISSUE PRESENTED

Whether Tax Code administrative exclusivity violates the Open Courts Guarantee (Tex. Const. art. I, § 13) when applied to bar district court jurisdiction over constitutional claims that the Appraisal Review Board lacks statutory authority to remedy.

III. STATEMENT OF JURISDICTION

The Court has jurisdiction under Tex. Gov't Code § 22.001(a). This case presents a constitutional question of first impression affecting millions of Texas property owners: Whether administrative exclusivity can constitutionally foreclose all judicial review of systematic constitutional violations when the administrative body lacks remedial authority to address such violations.

The decision below conflicts with this Court's precedent:

- LeCroy v. Hanlon, 713 S.W.2d 335, 341 (Tex. 1986), holds that the Open Courts Clause requires a remedy for every recognized legal injury. The Court of Appeals' holding eliminates any remedy—administrative or judicial—for systematic constitutional violations.

- City of El Paso v. Heinrich, 284 S.W.3d 366, 372 (Tex. 2009), holds that "suits to require state officials to comply with statutory or constitutional provisions are not prohibited by sovereign immunity." The decision below forecloses such suits through application of administrative exclusivity.

- Hensley v. State Comm'n on Judicial Conduct, 692 S.W.3d 184, 194 (Tex. 2024), holds that administrative exhaustion is not required when the administrative body cannot grant the requested relief, as exhaustion would be "a pointless waste of time and resources."

This issue affects all 254 appraisal districts statewide and the constitutional rights of Texas's 30 million property taxpayers. Resolution by this Court is necessary to clarify the relationship between administrative exclusivity provisions and constitutional guarantees of judicial review.

IV. STANDARD OF REVIEW

This Court reviews constitutional questions de novo. Patel v. Tex. Dep't of Licensing & Regulation, 469 S.W.3d 69, 75 (Tex. 2015).

Whether administrative exclusivity violates the Open Courts Guarantee is a pure question of law subject to de novo review. LeCroy v. Hanlon, 713 S.W.2d 335, 341 (Tex. 1986).

Whether a plea to the jurisdiction should be granted is likewise reviewed de novo. Tex. Dep't of Parks & Wildlife v. Miranda, 133 S.W.3d 217, 226 (Tex. 2004).

Because this case was dismissed at the pleading stage, all well-pleaded facts are taken as true. Tex. Ass'n of Bus. v. Tex. Air Control Bd., 852 S.W.2d 440, 446 (Tex. 1993).

V. STATEMENT OF FACTS

Petitioners allege that the Denton Central Appraisal District (DCAD) implemented a systematic mass appraisal methodology that violates Article VIII, Section 1(a)'s equal and uniform taxation mandate across all 455,000 properties in Denton County.

Petitioners do not challenge individual property valuations. Rather, they challenge the constitutional validity of DCAD's countywide methodology and seek declaratory and injunctive relief requiring DCAD to comply with constitutional requirements in all future appraisals.

The Appraisal Review Board's Authority Is Limited

The Appraisal Review Board's statutory authority is strictly limited to adjusting individual property valuations for single tax years. Tex. Tax Code § 41.02.

The ARB has no statutory authority to:

- Declare a mass appraisal methodology unconstitutional;

- Enjoin future use of unconstitutional methodologies;

- Order systematic changes to appraisal practices; or

- Provide relief affecting properties countywide.

See Tex. Tax Code §§ 41.01-41.47 (defining scope of ARB authority).

Procedural History

The trial court dismissed Petitioners' claims on sovereign immunity grounds, holding that the Tax Code's administrative remedies are exclusive.

The Court of Appeals affirmed, holding that Tax Code administrative remedies are exclusive regardless of the constitutional nature of the claims or the ARB's inability to grant the requested relief.

The Court of Appeals acknowledged that its holding forecloses Petitioners' access to any forum—administrative or judicial—capable of granting the prospective, systematic relief they seek.

VI. SUMMARY OF THE ARGUMENT

This Court should grant review to resolve a fundamental conflict between administrative exclusivity and constitutional guarantees of judicial review.

The Court of Appeals created an unconstitutional remedial gap. It acknowledged that Petitioners allege systematic constitutional violations affecting 455,000 properties, yet held that the only available forum is an administrative body (the ARB) that lacks statutory authority to remedy systematic violations or grant prospective injunctive relief.

This holding violates the Open Courts Clause (Tex. Const. art. I, § 13), which guarantees that "every person for an injury done him...shall have remedy by due course of law." When an administrative body is statutorily prohibited from granting the relief necessary to remedy a constitutional injury, that body cannot provide an adequate—much less exclusive—remedy.

The decision also conflicts with this Court's precedent:

- Heinrich establishes that constitutional compliance claims are not barred by immunity. Administrative exclusivity cannot accomplish indirectly (foreclosing constitutional claims) what immunity cannot accomplish directly.

- Hensley holds that exhaustion is not required when the administrative body lacks authority to grant requested relief. The ARB cannot grant systematic, prospective relief.

- LeCroy requires a remedy for every legal injury. The decision below provides no remedy for systematic constitutional violations.

VII. ARGUMENT

A. The Decision Below Violates the Open Courts Guarantee (Tex. Const. Art. I, § 13)

The Open Courts Clause provides: "All courts shall be open, and every person for an injury done him, in his lands, goods, person or reputation, shall have remedy by due course of law." Tex. Const. art. I, § 13.

This constitutional guarantee prohibits the Legislature from abolishing a remedy for a recognized legal wrong unless a reasonable substitute is provided or the abolition serves a legitimate state interest. LeCroy v. Hanlon, 713 S.W.2d 335, 341 (Tex. 1986).

The ARB Cannot Provide the Remedy Required for Systematic Constitutional Violations

Petitioners allege a systematic, countywide constitutional violation: that DCAD's mass appraisal methodology violates Article VIII, Section 1(a)'s mandate for equal and uniform taxation.

The relief necessary to remedy this systematic violation is: (1) A declaration that DCAD's methodology is unconstitutional; and (2) A prospective injunction requiring DCAD to implement constitutionally compliant appraisal methods in future years.

The ARB cannot provide this relief. The ARB's statutory authority is strictly limited to "direct[ing] the chief appraiser to correct or change the appraisal records or the appraisal roll" for individual properties. Tex. Tax Code § 41.02(a). The ARB has no authority to declare governmental conduct unconstitutional or issue injunctions against government officials.

A Remedy That Cannot Reach the Scope of the Injury Is No Remedy at All

The Open Courts Clause requires a remedy adequate to address the injury alleged. When a constitutional injury is systematic and prospective, and the administrative body lacks authority to grant systematic, prospective relief, the administrative process cannot provide an adequate remedy.

This Court has consistently held that a purported remedy is inadequate if it cannot address the nature of the injury:

- In Mellard v. Hammer, this Court emphasized that the Open Courts Clause requires "a remedy adequate to redress injury." 477 S.W.3d 125, 129 (Tex. 2015).

- In Hensley, this Court held that requiring exhaustion of an administrative remedy that cannot grant requested relief would be "a pointless waste of time and resources." 692 S.W.3d at 194.

Applying administrative exclusivity to bar district court jurisdiction when the administrative body cannot remedy the alleged constitutional injury violates the Open Courts guarantee by eliminating any adequate remedy.

B. The Decision Conflicts With This Court's Holding in Heinrich

In City of El Paso v. Heinrich, this Court unambiguously held that "suits to require state officials to comply with statutory or constitutional provisions are not prohibited by sovereign immunity." 284 S.W.3d 366, 372 (Tex. 2009) (emphasis added).

The decision below conflicts with Heinrich by holding that administrative exclusivity—a statutory creation—can bar constitutional compliance claims seeking to compel governmental adherence to constitutional mandates.

Administrative exclusivity cannot accomplish indirectly what sovereign immunity cannot accomplish directly: the foreclosure of constitutional compliance claims. If a legislature can eliminate judicial review of constitutional claims simply by creating an administrative process—even an inadequate one—Heinrich's guarantee becomes meaningless. This conflict requires this Court's resolution.

C. Administrative Exhaustion Cannot Be Required When the Administrative Body Lacks Authority to Grant Constitutional Relief

This Court has recognized that administrative exhaustion is not required when the administrative body lacks authority to grant the requested relief, when exhaustion would be "a pointless waste of time and resources," or when constitutional rights are at stake. Hensley v. State Comm'n on Judicial Conduct, 692 S.W.3d 184, 194 (Tex. 2024); Patel v. Tex. Dep't of Licensing & Regulation, 469 S.W.3d 69, 87-88 (Tex. 2015).

All these exceptions apply here. Requiring Petitioners to exhaust ARB remedies would be pointless because the ARB cannot declare DCAD's methodology unconstitutional, cannot enjoin future constitutional violations, and can only adjust individual valuations annually. Requiring exhaustion of a remedy that cannot provide constitutional relief violates due process and the Open Courts guarantee.

D. This Case Presents a Constitutional Question Distinct From Routine Tax Valuation Disputes

The Court of Appeals treated this case as a routine tax dispute subject to administrative exclusivity. But Petitioners do not challenge individual property valuations—they challenge the constitutional validity of DCAD's systematic methodology applied countywide.

This distinction is critical:

ROUTINE TAX DISPUTE (ARB Jurisdiction)

- Individual property owner challenges appraisal of his property

- Seeks adjustment of that specific property's value

- Relief sought is retrospective (correction of current year)

- ARB has statutory authority to grant relief (Tex. Tax Code § 41.02)

SYSTEMATIC CONSTITUTIONAL CHALLENGE (District Court Jurisdiction)

- Taxpayers challenge methodology affecting all 455,000 properties

- Seek declaration that methodology violates Art. VIII, § 1(a)

- Seek prospective injunction against future constitutional violations

- ARB lacks statutory authority to grant relief

Failing to recognize this distinction would eliminate judicial review for all systematic constitutional violations in tax administration. The Constitution does not permit executive branch agencies to implement systematic constitutional violations immune from judicial scrutiny.

E. Petitioners Challenge Administrative Exclusivity As Applied, Not Facially

Petitioners do not argue that Tex. Tax Code § 42.09 is facially unconstitutional. Administrative exclusivity is valid and serves important purposes when applied to disputes within the ARB's statutory competence—individual valuation challenges for specific tax years.

Petitioners argue that § 42.09, as applied to bar district court jurisdiction over systematic constitutional violations that the ARB cannot remedy, violates the Open Courts Guarantee.

This as-applied constitutional challenge preserves the Legislature's authority to channel routine tax disputes to administrative review while ensuring judicial protection of constitutional rights that exceed administrative authority.

F. The Decision Creates a Dangerous Precedent With Statewide Implications

If the decision below stands, it establishes that the Legislature can immunize executive branch agencies from judicial review of systematic constitutional violations simply by creating an administrative process—however inadequate—to address individual disputes.

The implications are staggering. Every executive branch agency with an administrative review process would be insulated from judicial review of its systematic practices, regardless of constitutional violations. This Court has never countenanced such a result. The Constitution requires judicial review of systematic governmental violations of constitutional rights, regardless of whether an administrative process exists to address individual grievances.

VIII. PRAYER FOR RELIEF

WHEREFORE, Petitioners respectfully pray that this Court:

- GRANT this Petition for Review;

- REVERSE the judgment of the Court of Appeals and HOLD that: a. Tax Code administrative exclusivity does not bar district court jurisdiction over claims of systematic constitutional violations when the Appraisal Review Board lacks statutory authority to remedy such violations; b. The Open Courts Guarantee (Tex. Const. art. I, § 13) requires judicial review of systematic constitutional violations that administrative bodies cannot remedy; c. Constitutional compliance claims, as recognized in City of El Paso v. Heinrich, 284 S.W.3d 366, 372 (Tex. 2009), are not subject to administrative exclusivity when the administrative body lacks authority to compel constitutional compliance; and d. Petitioners have stated viable constitutional claims not subject to dismissal on jurisdictional grounds;

- REMAND this cause to the trial court for proceedings on the merits consistent with this Court's opinion; and

- Grant such other and further relief, at law or in equity, to which Petitioners may be justly entitled.

Respectfully submitted,

As I have stated, either the law exists or it doesn’t. The ramifications of no law and systemic institutionalized moral hazard are frightening.