Forensic Audit of a Central Appraisal District

Taxpayers who know something is wrong with the appraisal practices & property valuations within their appraisal district should push for a Forensic Audit.

Provided here is a suggested guideline for the Scope of Work Letter between the Forensic Accountant and the Central Appraisal District’s (CAD’s) Board of Directors.

[Note: substitute date and names.]

February 3, 2026

ABC Central Appraisal District (ABCCAD)

Chairman, John Doe

and

Jane Smith, Certified Forensic Accountant or Fraud Examiner

DEF Forensic Accountants (Company Name)

Statement:

In recognition of possible criminal activity at ABCCAD by prior Chief Appraiser, Board Members, Employees, and associated licensing entities including but not limited to Texas State Comptroller, TDLR, TALCB, IAAO, TAAO, ABCCAD has found it necessary to hire a Forensic Accountant whose role and responsibility in this hiring are defined herein.

A forensic accountant is a financial expert proficient in carrying out investigations into financial discrepancies, fraudulent activities, and complex transactions.

Their expertise is often sought after in legal proceedings and disputes that involve financial issues, contributing an additional layer of scrutiny to our financial systems which include the CAMA software and additional software such as Excel, Email, PowerPoint, written communications and social media being utilized by ABCCAD, its employees and the School Districts and Municipalities, which are the Taxing Entities.

The Forensic Accountant will meticulously examine financial records, along with other data and records, for evidence of white-collar crimes such as embezzlement, money laundering, securities fraud, violations of Uniform Standards of Professional Appraisal Practice, Texas Property Tax Code, Texas Constitution, and U.S. Constitution including but not limited to:

A. Review of Possible Violations

B. Preparing a Summary Checklist & Identify Broader Implications of the Violations

C. Review of Underlying Factors Resulting in Violations

SECTION A – Review of Possible Violations

Have there been violations made by the ABCCAD and its employees?

[Attention Reader: Items in blue are examples of known violations.]

Violations of Mass Appraisal Standards (USPAP Standards 5 & 6)

1. Violated USPAP Records Keeping Rule when conducting mass appraisal.

- Failed to maintain work file in manner required.

2. Failed to comply with Ethics Rule by willfully/knowingly violating Records Keeping Rule.

- Violation of Record Keeping = Violation of Ethics.

3. Failed to comply with USPAP 5-1(a) by not correctly employing recognized techniques necessary to produce a credible mass appraisal.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices)

4. Failed to comply with USPAP 5-1(b) by committing substantial errors of omission and commission that significantly affected mass appraisal conducted by ABCCAD.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices)

[ NOTE TO READER:

YES… the list of examples may be the same for many of the violations. This further demonstrates the compound cumulative nature, or the ripple effect, of using a single improper analysis, or using a single improper figure, or using a single improper method, etc., etc. Read carefully what has been violated and then read an example of how violation was identified. If subject property is improperly valued, then so are many others, one improper analysis or assumption leads to many other improper ones. And with this many (volume) violations and improper valuations, was this done by intent, was it orchestrated?

END OF NOTE]

5. Failed to comply with USPAP 5-1(c) by rendering mass appraisal in careless or negligent manner.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices) - All of above demonstrate Appraisals (Notices of Appraisal) were completed in a careless & negligent manner, failing to use due diligence & due care.

6. Failed to comply with USPAP 5-2 (e)(iii) by failing to consider location & economic characteristics when conducting mass appraisal.

- Specific to a retail property has location and or exposure issues that have been documented by photos and by discussion with ABCCAD over many years.

- ABCCAD also failed to consider historical pattern and on-going economic characteristics supported by sub-par & low performing operating statements and well below average lease occupancy compared to other/most centers.

7. Failed to comply with USPAP 5-2 (k) by failing to determine scope of work to produce credible assignment results (appraisal values).

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices)

8. Failed to comply w USPAP 5-4(b) by failing to develop mathematical models that w/ reasonable certainty, represent relationship between property value and supply and demand factors as represented by quantitative & qualitative approaches to value for mass appraisal.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices) - All of above demonstrate Appraisals (Notices of Appraisal) were completed without a sound or well- developed model that with reasonable certainty, represent property value using quantitative & qualitative approaches to value.

9. Failed to comply w USPAP 5-4(b) by failing to employ recognized techniques for specifying property valuation models used.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices) - With all of the above identified as an issue with ABCCAD’s appraisal process, proper techniques have not been employed in valuation models.

- Specific to commercial shopping centers, ABCCAD has failed to use data obtained from the commercial shopping centers, year after year, to perform an objective income approach valuation for the Notices of Appraisal issued, or to be issued.

- As evidenced by many protest experiences, for homeowners, ABCCAD has also failed to perform uniform & equal (equity) valuations and sales comparison valuations prior to Notices of Appraisal being issued. ABCCAD subsequently produces such valuations as part of a homeowner’s protest process, where the comparable properties may not be comparable, and then offers to settle with homeowner for a value that has nothing to do with the new evidence and values they just produced for the protest.

10. Failed to comply w USPAP 5-4(c) by failing to employ recognized techniques for calibrating the mass appraisal models used.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices) - With all of the above identified as an issue with ABCCAD’s appraisal process, proper techniques have not been employed to review, test or calibrate the mass appraisal models.

- More detailed evidence of this violation may include reviewing the results a Standard Deviation Analysis of subject property as the base versus the CAD’s selected comparables and versus its true comparables.

11. Failed to comply w USPAP 5-7(a) by failing to reconcile the quality and quantity of data available and analyzed within the approaches used and the applicability and relevance of the approaches, methods & techniques used in mass appraisal.

- Absence of Uniform & Equal standard being applied.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

12. Failed to comply w USPAP 5-7(b) by failing to use or implement appraisal testing procedures and techniques to ensure that standards of accuracy are maintained for mass appraisal.

- Failed to employ testing procedures to ensure accuracy of valuations, as that would have required objective review of current year & prior year data to assist in establishing current year values.

- How does ABCCAD test for accuracy on dirty data, or fabricated data, used to purposefully inflate value?

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

13. Failed to comply w USPAP 6 by reporting the results of ABCCAD mass appraisal in a manner that is misleading.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices)

Violations of USPAP, Professional Appraisal Practice Rules

1. Violated USPAP Records Keeping Rule while working on commercial shopping centers values.

- Failed to maintain work file(s) in manner required.

2. Failed the Ethics General Rule.

- Individual appraisers and ABCCAD, have not promoted & preserved public trust inherent in appraisal practice.

3. Failed to comply with Ethics Rule of Conduct.

- Individual appraisers and ABCCAD willfully & knowingly violated Record Keeping Rule.

4. Failed to comply with Ethics Rule of Conduct.

5. Failed to comply with Ethics Rule of Management.

- Have the individual appraisers (and ABCCAD) disclosed a fee, commission or thing of value received in connection with appraisal/assignment?

6. Failed to comply with Ethics Rule of Management.

- Individual appraisers and ABCCAD have performed an assignment & issued Notices of Appraisal where the opinion of value was based on a predetermined result.

7. Failed to comply with Ethics Rule of Confidentiality.

- Individual appraisers and ABCCAD have not acted in good faith with regard to the legitimate interests of the client(s) (taxpayers & tax jurisdictions) in the use of confidential information and in the communication of assignment results.

- Individual appraisers and ABCCAD did not take reasonable steps to safeguard access to confidential information and assignment (appraisal) results that was in electronic form.

8. Failed to comply with Competency Rule.

- Individual appraisers and ABCCAD either do not possess the knowledge & experience to complete appraisal competently, or they are willfully not using proper appraisal knowledge & skills to complete appraisals.

9. Failed to comply with Competency Rule.

- Individual appraisers and ABCCAD have not recognized or complied with laws & regulations that apply to appraiser or to the assignments (the tax appraisals).

10. Failed to comply with Scope of Work Rule.

- Must demonstrate that scope of work is sufficient to produce credible assignment results (appraisals)

- Improper research and or application of research & techniques, improper analysis applied to arrive at opinion or conclusion.

11. Failed to comply with Jurisdictional Exception Rule.

- ABCCAD cannot make this exception, Texas Property Code requires that ABCCAD use USPAP.

Violations of USPAP, Standards & Standard Rules, 1 and 2

1. Standards Rule 1-1, General Development Requirements, violations:

- Fail to employ methods or techniques to produce credible appraisals.

- Have committed substantial errors that significantly affect appraisals.

- Have rendered appraisal in a negligent manner, affecting results of values across Appraisal District/County.

- Ignored prior year(s) data collected & prior year(s) protest/appeal reductions.

- Inserted improper data on Income Calculation Worksheets (for commercial property).

- Inserted improper data into Comparison Grids (for commercial property or residential property)

- Failed to use actual/proper comparable properties.

- Issued improper Notices of Appraisal.

- Created high volume of protests & high percentage value reductions from protests and appeals.

(specific example: commercial shopping center sample of 140, over 90% protested & received average reduction of over 30%)

(specific example: over 90% of all commercial property owners & over 40% of all homeowners protest their appraisal notices)

2. Standards Rule 1-2, Problem Identification, violated subsections e & h:

e) did not identify characteristics of property that are relevant to type & definition of value & failed to use reliable information when available.

h) did not determine scope of work to produce credible assignment results.

3. Standards Rule 1-4, Approaches to Value, violated:

- Violated general rule (and subsections): Have not analyzed or utilized the actual data provided year after year to produce a credible assignment result (appraisal) on the Income Approach for commercial property valuations; have not consistently used truly comparable properties for sales comparison approach or the equity (equal & uniform) approach.

4. Standards Rule 1-6, Reconciliation, Subsection a violated:

a) have not used all the “quality” data (all the actual data) in analysis or valuation approaches and have not reviewed their proposed values & data to verify accuracy for/on values set on Notices of Appraisal.

Standard 2: Real Property Appraisal, Reporting

5. Standards Rule 2-1, General Reporting Requirements, Subsections a & c violated:

a) failed by misleading taxpayers on Notices of Appraisal (evidenced by volume of protests & appeals).

c) have in essence claimed extraordinary assumptions for most, or all, taxpayers, by issuing high values on Notices of Appraisal without proper comparable (uniform & equal) evidence, or proper support of increased value due to higher/enhanced “economic characteristics.”

6. Standards Rule 2-2, Content of Real Property Appraisal Report, violated:

- Have violated content rule by misleading taxpayers with the value issued on the Notice of Appraisal.

7. Standards Rule 2-3, Certification, violated:

- There is no signed certification to taxpayer, but there is a certification to taxing jurisdictions who empower ABCCAD to do tax valuations/appraisals.

- Certification rule is violated because values are not true & correct; analysis is not accurate or unbiased; engagement is contingent on predetermined results; analysis, opinions & conclusions are not conforming with USPAP.

8. Standards Rule 2-4, Oral Appraisal Report, violated:

- ABCCAD is in violation of USPAP rules with the Notice of Appraisal issued, the reports provided in protest hearing, and their verbal testimony of value with taxpayer & ARB panel, as if their opinion of value is fact.

Violations under TDLR

(Texas Administrative Code, Title 16 - Economic Regulation, Part 4 - Texas Department of Licensing & Regulation, Chapter 94 – Property Tax Professionals)

94.70 – responsibilities of a registrant – general

- Registrants cannot violate any provision.

- Registrants must not violate property tax professional code of ethics.

- Registrants must not engage in any practices that constitute improper influence, conflict of interest, unfair treatment, discrimination, abuse of power or misuse of titles.

94.71 – responsibilities of a registrant – equal & fair treatment

- Registrants must apply equally & fairly any appraisal or assessment according to USPAP & generally accepted appraisal or assessment practices applicable.

- Registrant must not knowingly testify falsely or withhold any information, or influence someone to do so, in any investigation or proceeding.

- Registrant must not knowingly mislead any member of the public who makes reasonable inquiry or request on tax matters.

- Registrant must not predetermine the value or value range of a property or properties and then manipulate data to arrive to a predetermined conclusion (value).

94.72 – responsibilities of a registrant – conflicts of interest

- Registrant must disclose in writing to appraisal district or taxing entity any financial interest in any private business or real property subject to appraisal district or taxing entity where he/she is employed.

- Registrant must not use any agency resources for personal benefit.

94.100 – code of ethics

- Registrant must be guided by principal that property taxation should be fair and uniform, and apply all laws, rules, methods, procedures, in a uniform manner, to all taxpayers.

- Registrant must not accept or solicit any gift, favor or service that might reasonably tend to influence registrant in the discharge of official duties.

- Registrant must not engage in an official act that is dishonest, misleading, fraudulent, deceptive, or in violation of law.

- Registrant must not conduct their professional duties in a manner that could reasonably be expected to create the appearance of impropriety.

Violations of Texas Property Tax Code

Chapter 23, Appraisal Methods & Procedures:

Sec 23.01 (b) (2nd clause/rule of Chapter 23) violated.

- If appraisal district determines appraised value of property using mass appraisal standards, the mass appraisal standards must comply with USPAP. Same or similar appraisal methods & techniques shall be used in appraising the same or similar kinds of property. However, each property shall be appraised based on the individual characteristics that affect the property’s market value, and all available evidence that is specific to the value of property shall be taken into account in determining the property’s market value.

- Violating the uniform & equal (comparable/median value/10% rule), but a basic and general rule, as they continue to ignore actual property performance data provided year after year when applying it to the Income Calculation Worksheet (the income approach).

Sec 23.012 Income Method of Appraisal violated. (used with commercial property)

- This section states that ABCCAD can use comparable (trends & averages of others) income & expense data in valuing commercial property. This doesn’t mean they can pull an expense figure out of thin air. Example, using an operating expense number of $24,910 (or $2/sf) for subject shopping center is OBVIOUSLY not comparable data, when it is only one third the subject’s historical average. Figure is not historically accurate, nor a proper historical estimate of subject, and is not an objective or historical average operating expense for other comparable properties. The $24,910 ($2/sf) was supposed to represent all property operating expenses outside of, or except for, property tax and interest and $2/sf does not.

Sec 23.013 Market Data Comparison Method of Appraisal violated.

- ABCCAD violates Sec 23.013 (a) by NOT using comparable properties in analysis of sales (market value).

Sec 42.26, Remedy for Unequal Appraisal violated.

- ABCCAD violates Sec 42.26 by issuing value(s), and or not reducing value(s) in protest hearing, to a taxable value within 10% of the median value/sf of a group of comparable properties.

Violations of TALCB, Texas Appraiser Licensing & Certification Board

Violations under USPAP or TDLR are violations under TALCB.

SECTION B – Prepare a Summary Checklist & Identify Broader Implications of the Violations

Fraud at ABCCAD check list:

- State(s) Property Tax Codes Violated: must comply with Uniform Standards of Professional Appraisal Practice (USPAP).

- Violated Rule 5-1(a): not correctly employing recognized techniques to produce a credible mass appraisal

- Violated Rule 5-1(b): committing substantial error of omission & commission that significantly affect mass appraisal

- Violated Rules 5-1(c): rendered mass appraisal in a careless & negligent manner

- Violated Texas Property Tax Code 23.01(e): must use "clear and convincing evidence"

- Violated Texas Property Tax Code 23.012, Income Method of Appraisal: ignored and fraudulent income statements created

- Violated Texas Property Tax Code 23.013: have not used TRUE like-kind properties when using sales data to render value

- Violated Texas Property Tax Code 42.26: remedy for unequal appraisal, must be within 10% of median value of comparisons

- Violated Texas Constitution Article 8, Section 1(a): property taxation (valuation) is not equal and uniform as required

- Violated Texas Constitution Article 8 Section 20: properties valued for ad valorem higher than fair cash market value

- Violated Texas Property Tax Code Chapter 5 Section 5.01: State has not taken responsibility for appraisal district(s) who failed to follow law in property tax appraisal process.

- Violated Texas Property Tax Code Chapter 5 Section 5.04: State nor TDLR takes responsibility for failed standards

- Tax Roll Certification was FALSIFIED

- TDLR, Texas Administrative Code Chapter 94, Regulations for Property Tax Professionals: Violated, "No Enforcement"

- TALCB, Texas Appraiser Licensing & Certification Act, Chapter 153: Violated, "No Enforcement"

- Property Valuation Study (PVS) at the hands of the State Comptroller is a fraudulent mechanism used to raise property values to move funds between school districts to drive property values higher at the demand of the State Comptroller

- Oath of Profession, violated when code of ethics and laws are broken, including TDLR, TALCB, professional organizations, IAAO, TAAO, Real Estate Foundation, etc.

- Oath of Office violated: not following laws, many individuals failed at their duties, Chief Appraiser, Board Members, ARB members.

- Texas Penal Code 37.11- Violated by defaulting in duties as public official is impersonating a public official 3rd degree felony

- Texas Penal Code 7.01 – Violated, intentionally failed to report criminal activity

- Texas & U.S. Administrative Procedures Act – Violated

- U.S. Constitution 1st, 5th, 14th, 16th Amendments – Violated

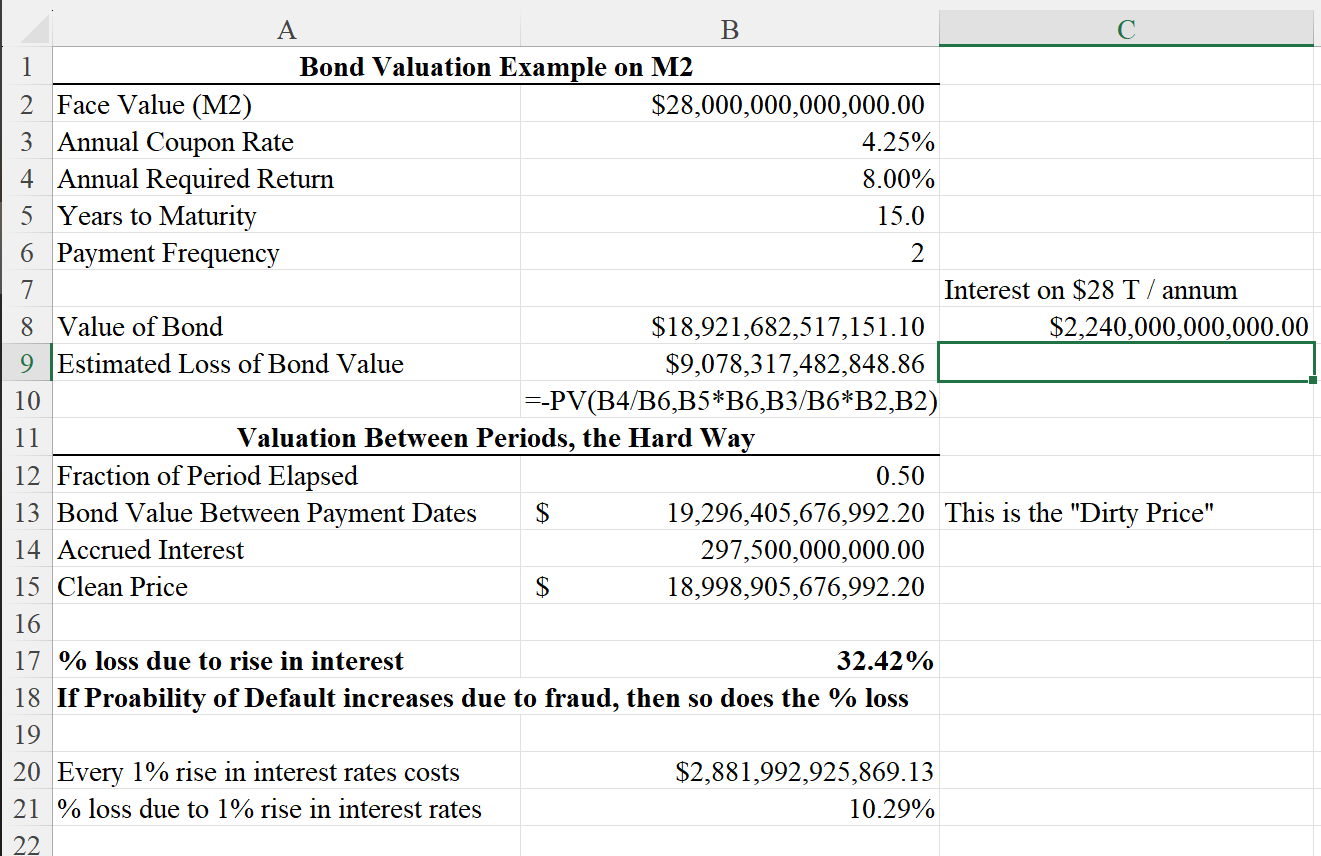

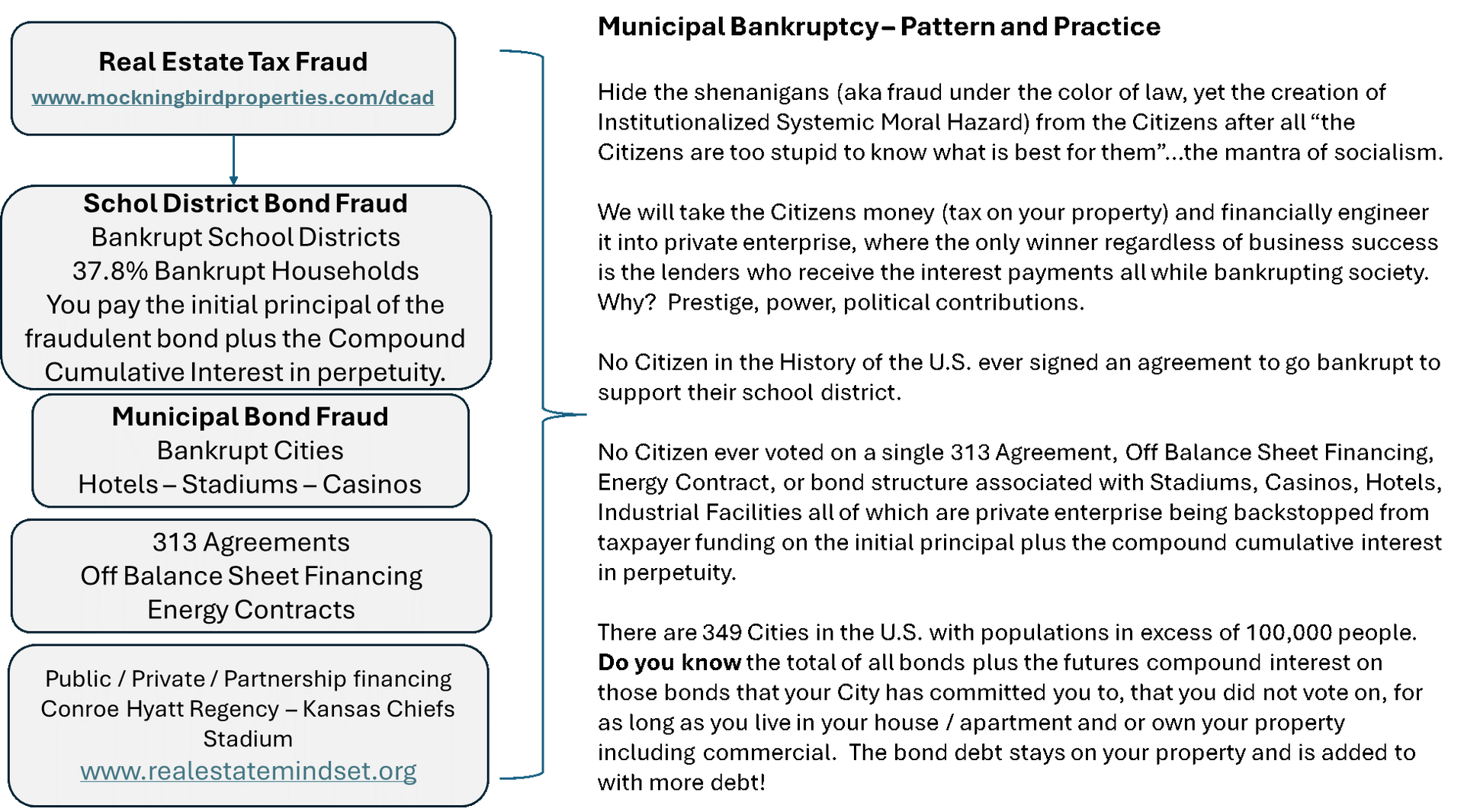

- School District Bond values based on the "implicit guarantee" of the real estate taxpayers, not true value under law

- Bond investors i.e. 401K and Pensions are at considerable risk due to overvaluation and over taxation by the CADs

- VIOLATED Title 42 U.S. Code Section 1986, Knowledge of Wrongful Act & Power to Prevent

- VIOLATED Title 18 of Criminal Code, U.S. Code Section 1621, Perjury Defined

- VIOLATED Title 18 U.S. Code Section 1512 c 1 2, who corruptly alters. Destroys or conceals a record (violations of RICO at State and Federal Levels

SECTION C - Review of Underlying Factors Resulting in Violations

Did the Tax Assessor Collector receive corrupt certifications from ABCCAD?

Was USPAP followed when performing Mass Appraisals?

Was the Initial Notie of Value fraudulent because the value was determined by not adhering to USPAP?

If the data was determined by not adhering to USPAP, and comparisons were created off of the corrupted data, then is it a fair statement that 76%+ of the database is corrupted?

Does the current property tax system as determined by intent, have a circular argument in that ABCCAD gives Certified Totals to the State Comptroller PTAD, where the State Comptroller, under law, is charged with “regulating the administration of property taxation,” including establishing and overseeing the CADs, in addition to providing technical assistance, yet, the State claims no authority of enforcement and has directed complaints be handled by the local CAD (ABCCAD) or local district court?

USPAP guidance is provided by IAAO, TAAO, Appraisal Foundation, Appraisal Institute and others and it is recognized in law by the Comptroller. Is it a true statement that ABCCAD and related government agencies make claims, they follow USPAP, but the evidence shows they do not adhere to USPAP or the Texas Property Tax Code?

Does the Chief Appraiser at ABCCAD have discretion to ignore USPSP, Texas Property Tax Code, The Texas Constitution, or the Constitution of the United States of America?

Is ABCCAD an unlawful agency that must be enjoined under U.S.C. 706(s)(A)?

The above three sections (A), (B), and ( C), concerning ABCCAD and its employees, along with their Violations in Appraisal, Licensing, Property Tax Code, USPAP General and Professional Standards, Mass Appraisal Standards (USPAP Standards 5 & 6), and the frauds at ABCCAD, form a checklist of questions requiring answers and will then form the basis of your report and said report will provide backup evidence in corresponding order for each line item.

More Background on Fraud Detection & Prevention:

The Forensic Accountant is not only an expert in accounting but also an accomplished investigator. Their primary function is to thoroughly scrutinize financial records in search of anomalies or irregularities.

By conducting detailed audits, the Forensic Accountant will piece together a complete, accurate financial picture, effectively sifting through layers of financial data and corresponding written law to uncover potential fraud or misrepresentation.

The Forensic Accountant will use their findings to establish patterns of behavior that may indicate fraudulent activity following leads and investigating suspicious transactions.

Beyond just the numbers, the Forensic Accountant is to interpret the financial data in the broader context, identifying hidden relationships and unearthing clues which can unveil the truth behind a potentially deceptive financial façade. These potential hidden relationships include by and between ABCCAD, the school districts, and municipalities within the appraisal district area.

This scope of work as well as the report in its entirety will be made public for the purposes of full transparency.

Fraud Detection and Prevention:

Unmasking fraud and preventing it from reoccurring stands as one of the cornerstone responsibilities of forensic accountants.

These experts not only detect fraud but also design and implement measures to prevent future instances.

They work closely with organizations to strengthen internal controls, conduct regular audits, and educate employees about potential fraud schemes.

In this role, forensic accountants serve as the vanguards against financial malfeasance, contributing significantly to business longevity and integrity.

Duties and Responsibilities:

- In addition to answering the questions as outlined above, Investigate ABCCAD and associated entities and employee’s financial data including social network analysis, transaction flow diagrams, timelines, adherence to law (as outlined above), excel models, data mining software, statistical software, spreadsheets, computer forensic techniques and analysis of the CAMA (Computer Aided Mass Appraisal) software database logs of who made the entries, based on what USPAP and Mass Appraisal Standards criteria, and manipulation of the database files outside of the CAMA software. For purposes of speed and cost efficiency, Forensic Accountant may group (i.e. 100 examples of each) the analysis into:

A. Single Family Homes

B. Qualified Farm (AG) Land

C. Industrial Real Property

D. Retail Shopping Centers

E. Multifamily

F. Mobile Homes

G. Raw Land

H. Seniors Housing

With regard to the above grouping:

- Determine the percent swings (%) in values between property types utilizing Standard Deviation.

- Determine the non-uniformity of application of USPAP and Mass Appraisal Standards.

- Determine the change in land values as compared to the building values.

- For single family homes, determine the average debt to equity ratio for the median home price in its market area and appraisal district area and or county.

- Determine what percentage of the time the ARB panels agreed with ABCCAD’s value determination. (ARB Panels should be operating and acting independent of the appraisal district.)

- Determine the annual percentage increase of values for each of the categories above over the last 5 years. I.E. Year 2020, Single Family Total Units, SF total valuation, Average Cost er SF Unit.

- Determine what the pension liabilities are at ABCCAD, who receives what pension and based on what criteria.

- Obtain the one or more annual pre-determined budgets from one of more ABCCAD School Districts that was delivered to ABCCAD and or the Chief Appraiser. Determine if that School Districts has proper notes to their balance sheet, sources and uses, and bond schedule showing the payoff of prior bonds and the current status of all bonds being cost, due date, bond holder, bond issuer.

Determine if the following code sections were violated: (yes or no)

Violations of Texas Property Tax Code

- Texas Property Tax Code, 23.01(b), if failed basic directives for appraising value, including that it must comply w/ USPAP

- USPAP Standards 5 & 6, Mass Appraisal Standards, required by Property Tax Code

- USPAP Standards 1 & 2, Real Property Appraisal Development & Reporting, required by Property Tax Code

- USPAP Standard Appraisal Professional Rules, required by Property Tax Code

- Texas Property Tax Code, 23.01(e), if have not had “clear & convincing evidence” as required to increase value when prior year was reduced.

- Texas Property Tax Code, 23.01(f), if have not used TRUE like-kind properties (comparables) to render equitable value.

- Texas Property Tax Code, 23.012, Income Method of Appraisal, if ignored income property’s $$ performance data.

- Texas Property Tax Code, 23.013, if have not used TRUE like-kind properties when using sales data to render value.

- Texas Property Tax Code, 42.26, remedy for unequal appraisal, must be within 10% of median value of comparables.

- Texas Constitution, Article 8, Section 1, if property taxation (valuation) has not been equal & uniform as required.

- Texas Constitution, Article 8, Section 20, if properties have been valued for ad valorem purposes at a value higher than their “fair cash market value” by ABCCAD.

- Texas Property Tax Code, Chapter 5, Section 5.01, if State has not taken responsibility for appraisal district(s) who failed to follow law in property tax appraisal process.

- Texas Property Tax Code, Chapter 5, Section 5.04, if neither state nor TDLR has taken responsibility for failed training or failed application of professional & legal standards (laws).

Violations of USPAP, Standard Rules 1 & 2 (Real Property Appraisal: Development & Reporting)

1. Standards Rule 1-1, General Development Requirements, violated:

- Fail to employ methods or techniques to produce credible appraisals

- Committed substantial errors that significantly affect appraisals

- Rendered appraisal in a negligent manner, affecting results of values across Denton County

2. Standards Rule 1-2, Problem Identification, subsections e & h, violated:

- Did not identify characteristics of property that are relevant to type & definition of value

- Failed to use reliable information when available (even when in physical possession of it)

- Did not determine scope of work to produce credible assignment results

3. Standards Rule 1-4, Approaches to Value, violated:

- Have not analyzed or utilized actual data provided year after year to produce a credible assignment result (appraisal) on the Income

- Approach for commercial property valuations

- Have not consistently used comparable properties for sales comparison approach or the equity (equal & uniform) approach

4. Standards Rule 1-6, Reconciliation, Subsection a violated:

- Have not used all the “quality” data (all the actual data) in analysis or valuation approaches

- Have not reviewed or tested proposed values & data to verify accuracy for values on Notices of Appraisal

5. Standards Rule 2-1, General Reporting Requirements, Subsections a & c violated:

- Failed by misleading taxpayers on Notices of Appraisal (evidenced by volume of protests & appeals)

- Claimed extraordinary assumptions for most, or all, taxpayers, by issuing high values on Notices of Appraisal without proper comparable (uniform & equal) evidence, or proper support of increased value due to higher/enhanced “economic characteristics.”

- (SPECIFIC VIOLATION, sec 23.01(e) of Property Tax Code)

6. Standards Rule 2-2, Content of Real Property Appraisal Report, violated:

- Violated content rule by misleading taxpayers with the value issued on the Notice of Appraisal.

7. Standards Rule 2-3, Certification, violated:

- Provided values based on inaccurate analysis, manipulation & bias; completed appraisals contingent on predetermined results

- Failed to conform with USPAP throughout appraisal process, resulting in the issuance of inflated values on Appraisal Notices

8. Standards Rule 2-4, Oral Appraisal Report, violated:

- ABCCAD is in violation of USPAP rules with Notice of Appraisal issued and reports provided in protest hearing, making their verbal testimony of value with the taxpayer, the ARB panel members, or any other informal communication also a violation.

Violations of TDLR

(Texas Admin. Code, Title 16 - Economic Reg., Part 4 - Texas Dept of Licensing & Reg., Chap. 94 – Property Tax Professionals)

94.70 – responsibilities of a registrant – general

- Registrants cannot violate any provision.

- Registrants must not violate property tax professional code of ethics.

- Registrants must not engage in any practices that constitute improper influence, conflict of interest, unfair treatment, discrimination, abuse of power or misuse of titles.

94.71 – responsibilities of a registrant – equal & fair treatment

- Registrants must apply equally & fairly any appraisal or assessment according to USPAP & generally accepted appraisal or assessment practices applicable.

- Registrant must not knowingly testify falsely or withhold any information, or influence someone to do so, in any investigation or proceeding.

- Registrant must not knowingly mislead any member of the public who makes reasonable inquiry or request on tax matters.

- Registrant must not predetermine the value or value range of a property or properties and then manipulate data to arrive to a predetermined conclusion (value).

94.72 – responsibilities of a registrant – conflicts of interest

- Registrant must disclose in writing to appraisal district or taxing entity any financial interest in any private business or real property subject to appraisal district or taxing entity where he/she is employed.

- Registrant must not use any agency resources for personal benefit.

94.100 – code of ethics

(This is the section of regulations that TDLR Sr Investigator said TDLR may not have authority to enforce.)

- Registrant must be guided by principal that property taxation should be fair and uniform, and apply all laws, rules, methods, procedures, in a uniform manner, to all taxpayers.

- Registrant must not accept or solicit any gift, favor or service that might reasonably tend to influence registrant in the discharge of official duties.

- Registrant must not engage in an official act that is dishonest, misleading, fraudulent, deceptive, or in violation of law.

- Registrant must not conduct their professional duties in a manner that could reasonably be expected to create the appearance of impropriety.

2. Assemble and analyze evidence of criminal activity

3. Financial data interpretation and evaluation

4. Conduct interviews with personnel in order to uncover and collect evidence

5. Map a criminal hypothesis based on the information

6. Present the finding of the investigation to appropriate parties (Board of CAD, District Attorney, etc.)

7. Prepare documentation and evidence for court presentation

8. Clearly and professionally present evidence of financial irregularities and violations of law to appropriate parties.

9. Explain the research finding in layman’s terms and disclose investigative methods and procedures .

Litigation Support:

The forensic accountant will assist lawyers by providing a clear, concise interpretation of complex financial data as outlined above.

Expert Witness Testimony:

The forensic accountant may be called upon to present their findings in court, explaining complex financial concepts in a manner that judges, juries, and attorneys can comprehend.

Additional Scope of Work:

The above question from which answers are sought, form the basis of the hiring of this Forensic Accountant. Should it be determined between the parties that an additional avenue of investigation is necessary then at that time the parties may agree, in writing, to an addendum to this Scope of Work.

Agreed to this 3rd day of February 2026

By: John Doe

Chairman, ABCCAD Board of Directors

&

By: Jane Smith

Forensic Accountant

Professional Certifications attached