Co-Conspirators

State & Local Officials, Appraisal Districts, The Federal Reserve

By Mitchell Vexler, April 3, 2026

Link to Corresponding Graphics: The Architecture of Equity Stripping – The Red Ledger Audit

Roughly 37.6% which is 42,000,000 households in the U.S. are going to go bankrupt or lose the roof over their head. (See A Bankrupt Population is a National Security Risk.)

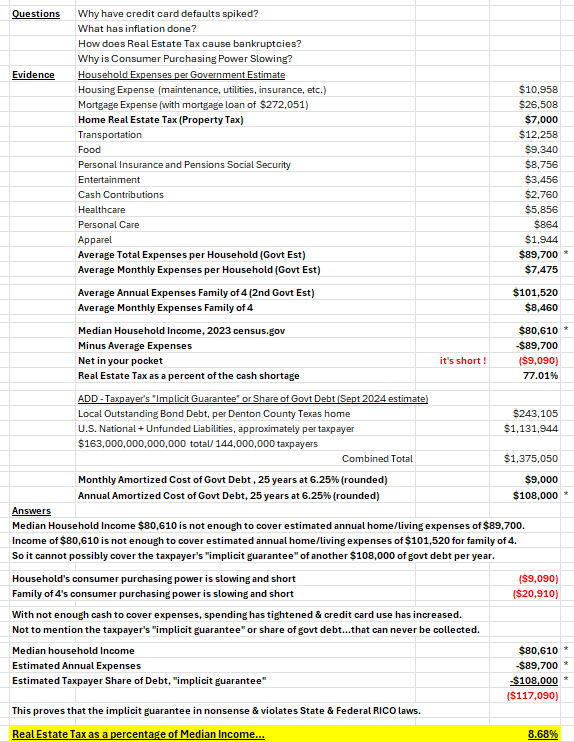

The true house affordability is $103,000 based on today’s Median Household Income (MHI) of $81,000 and average expenses, including the fraudulent real estate taxes at roughly $7,000 /year, assuming $50,000 cash down, meaning the difference of $43,000 in purchasing power. At $7,000 per year, the real estate tax fraud component is roughly $583/month. Graphic provided below. (Also, see Review of Home Affordability of Denton County Texas for 2023.)

There are 3147 counties in the U.S.

34 states and the District of Columbia have accessed the tax-exempt bond market to finance their schools.

- https://duckduckgo.com/?q=how+many+counties+in+the+US+raise+bonds+for+theirnschools&t=ipad&ia=web&assist=true

- https://report.lisc.org/charter-school-bond-study/issuance-by-state

Bond election fraud has occurred. The voters don’t have a clue about the reverse amortization and equity stripping they were duped into. Argyle Texas has roughly $243,000 per household in outstanding fraudulent school district bond debt.

The evidence of accounting fraud and thus bond fraud is also shown in multiple independent reports from across the U.S. including:

- JCAD Comprehensive Report

- JCAD and GISD violations of Law

- California Policy Center – Bond Study – including bond election fraud

- Residential Appraisal Testimony

- 313 Agreements, Energy Contracts, Off Balance Sheet Financing (CommonSenseLaw.org)

- Conroe Hyatt Regency Convention Hotel - Bond (PPP) Financing

(or see article,Municipal Bankruptcy) - School Funding Issues- BOND FRAUD

(use find, search for “bond” onhttps://www.mockingbirdproperties.com/dcad)

The only reason housing is not affordable is because of the fraud that allowed for overvaluation and over taxation and the fraudsters and co-conspirators that are responsible.

The databases are intentionally and irretrievable corrupted.

There would need to be a 40-50% house price reduction just to get back to the value where we were 6 years ago. According to the Fed, inflation only ran at roughly 3% per year for that period, 2020 to 2025. That’s about 18%. House values have gone up an average of 100% across the U.S. That means 82% of the increase is pure fraud for a variety of purposes, the majority of which is the interest on school district bonds, and this means the bonds have not been paid off but rolled out in time and the interest rates rolled up and this has been happening since at least the year 2000. Add into this, the rule of 72 till today, plus the annual increase in demand for more school district bonds and the amortization schedule that you are being demanded to pay for over the next 20 to 40 years, and it is an irrefutable fact that the school districts are bankrupt as are 42,000,000 households. The longer this deception plays out the larger the number of defaults.

School District Superintendents have committed accounting fraud and bond fraud.

USPAP (Uniform Standards of Professional Appraisal Practice) is required in law (Section 23.01(b) of the Texas Property Tax Code) and Uniform and Equal is required under the Texas Constitution. Both have been rendered meaningless by the fraud, as has the Appraisal Foundation.

Who is responsible…Chief Appraisers, School District Officials, the Boards, their attorneys as officers of the court who are aiding and abetting a criminal conspiracy to defraud, state comptrollers, AGs, IAAO, TAAO, inspector general, and the Judges that refuse to allow the prosecution of what has already been admitted as fraud.

What is the difference between Ilhan Omar, Chief Appraiser Don Spencer, and Jerome Powell?

- Ilhan Omar has allegedly stolen over $30 million by way of kickbacks and money laundering through a winery that does not exist, and that money is taxpayer money.

- Don Spencer, as Chief Appraiser of the Denton Central Appraisal District, is responsible for the over taxation of Denton County Taxpayers in excess of $1.34 Billion of taxpayer money stolen as a result of fraud in 2023, with over $7.17 Billion in excess tax from 2017 to 2025 by Spencer and his predecessors. (See Review of DCAD Certified Values & Property Taxes 2017 to 2025.)

- Jerome Powell’s term started in 2018 where the assets of the fed were roughly $4.4 Trillion. By 2023 they were $8.3 Trillion, and right now are at around $6.7 Trillion. Taxpayer money is being shuffled around.

All 3 of these people and their organizations are frauds, wherein your money is transferred into their pocket without a hope of ever seeing a return on, or return of, your money because the debt they created by virtue of fraud cannot be paid off but for printing of more money thus creating more fraud. At the local level, property values are increased fraudulently to generate more tax revenues and to support raising more municipal and school bonds in order to cover off the compound cumulative roller coaster of interest, the bigger fraud. Mom and Pop are the printing presses for the school districts, and the Fed is the printing press for the banks.

We have Mr. Spencer on tape stating that they took 60,000 properties outside of the database in excel, manipulated them, and put them back. This statement was delivered to the SCOTX.

Mr. Powell, I have only one question…and that is… how exactly is any of the U.S. National Debt going to be paid off, as in retired?

Mr. Spencer, I have the exact same question for you. How exactly are the property owners going to get back the billions you stole from them?

Mr. Powell has zero credibility. Remember “Inflation is Transitory”! Mr. Spencer and the entire DCAD operation also have zero credibility, and DCAD, along with all CADs, must be terminated as they are beyond repair.

We now have the attorney’s playbook (how to aid and abet a criminal conspiracy to defraud being used across the U.S.) wherein opposing counsel in the Vexler case through persistent lies, is asking the court(s) to guarantee taxation without representation. The exact circumstance that the War of Independence was fought over which was “NO Taxation Without Representation”. Opposing Counsel’s responses, being the playbook, are on my website. (See Response for DCAD & Response for Spencer at https://www.mockingbirdproperties.com/dcad)

The evidence is irrefutable, and insurmountable under the laws of the U.S. (See Violations.pdf.)

The laws of the U.S. and State Laws are not being adhered to in favor of fraud which ends up equity stripping all of society.

Math is the Achilles heal of socialism – Federal Reserve and School Districts are on the exact same rails of the train track. (See The Debt Model of socialism, Chain the Doors of the Federal Reserve, & We Don’t Need Arguments. We have Facts, Law & Math.)

The only thing that is holding this crime scene together is fraud.

NY City just received a negative bond rating. This problem has been building for over 50 years with regard to the pension fraud.

The reckoning is the fact that the Math will supersede the delay of the government’s interference in the natural course of your economics. The Math exposes the fraud and the co-conspirators, including the rating agencies. We laid the evidence at the feet of the DOJ, FBI, and SEC.

Private credit, private equity, shadow banks, big banks, all of which are cross collateralized, and leveraged into derivatives and a portion of your 401K and Pension is interwoven into this mess which also contains School District Bonds and Municipal Bonds.

The solution is the immediate repeal of all property tax in favor of the Uniform States Sales Tax which eliminates the “industry of fraud” and restores the 16th Amendment, being taxation on income only, and restores property ownership such that when the property is paid off you own it.

We are at the SCOTX now, asking to remand the case to the lower court to be heard on its merits of fraud.

The more people that know and participate the faster a proper resolution will occur. Forward the videos and links to the articles and to protect yourself and your family you must get involved at your municipal and school district levels. Your group should hire attorneys and prosecute the criminals, or 37.6% + of the people in this room will face bankruptcy. The heavy lifting is done; all you have to do is duplicate it. You have the power and you need to use it.

Go to…

- www.realestatemindset.org for how to do proper comparisons and file criminal complaints,

- www.mockingbirdproperties.com/dcad to review the depth of the issues, including reading Articles, Letters, and Discussions,

- www.commonsenselaw.org to learn about 313, energy contract and methods of kickbacks.

Take a camera and a witness to every interaction at a CAD, School District, and Municipal function. When they lie straight to your face, post it on social media.

The CAD are coconspirators with the school district.

Let’s look at the accounting for school district bonds.

THE BONDS WERE RAISED BASED ON MULTIPLE FRAUDS INCLUIDNG BUT NOT LIMITED TO:

A. Federal Reserve printing money which creates inflation, which is a tax, which is fraud on the Citizens.

- CENTRAL APPRAISAL DISTRICT OVERVALUATION AND OVER TAXATION WITH NO REGARD TO USPAP, TEXAS PROPERTY TAX CODE, TEXAS CONSTUTION AND THE CONSTITUTION OF THE UNITED SATES OF AMERICA.

- SCHOOL DISTRICT ACCOUNTING FRAUD AND SUBSEQUENT BOND FRAUD. A.) FALSIFYING DEMOGRAPHIC PROJECTS, B.) FALSIFYING COST TO BUILD WIHTOUT BIDS OR DRAWINGS C.) FALSIFYING COST TO OPERATE D.) HIDING INFORMATION ON “INVESTMENT POOLs”, E.) HIDING COST OF COMPOUND CUMULATIVE INTEREST ON OUTANDING BONDS, F.) HIDING ANY PROPER ACCOUNTING (FORENSIC AUDIT) SPECIFYING AND MATCHING THE BONDS RECEIVED TO THE SPECIFIC DEMAND FOR THE BOND G.) FALSIFYING ADVERTISING FOR THE RAISE OF THE BONDS H.) UTILIZING LUMP SUM ANNUAL BONDS WITH NO BREAKDOWN OF THE USES OF THOSE BONDS I.) NO AUDITS FOR THE SOURCES AND USES OF THE BONDS J.) NO CHECKS AND BALANCES “WE ARE NOT THE REPOSITORY OF DOCUMENTS” AS STATED BY THE OFFICE OF THE ATTORNEY GENERAL K.) “NO ENFORCEMENT” AS STATED BY THE STATE COMPTROLLER L.) UNDERWRITERS FRAUDULENTLY CLAIMING “UNLIMITED TAX” M.) RATING AGENCIES ARE GROSSLY NEGLIGENT N.) SCHOOL DISTRICT BALANCE SHEETS DO NOT REFLECT POPER ACCOUNTING FOR THE BONDS INCLUDING COMPOUND CUMULATIVE INTEREST BY NOT PAYING OFF THE BONDS BUT ROLLING THEM UP AND ROLLING THE INTEREST OUT AND IN ADDITION NOT ACCOUNTING FOR THE COST OF NEW BONDS ADDED TO THE PRIOR BONDS AND EXAMINING THE ABILITY OF THE HOUSEHOLDS TO PAY WHICH THE MAJORITY CANNOT BASED ON THE MEDIAN HOUSEHOLD INCOME.

B. The Real Estate tax includes the FED’s fraud, plus the fraud of overvaluation and over-taxation.

C. Now add the cumulative bond fraud at the school districts.

= THIS IS A PONZI SCHEME OF BIBLICAL PROPORTIONS.

- Jobs – where is the economic engine?

- Housing Inventory declining?

- Population declining?

- Seniors’ taxpaying ability declining?

- Student enrollment down? i.e. 8% in Itasca.

- Flatline population growth?

- Failing teachers and school districts, yet the demand for bonds goes unabated.

Why? Who receives benefit? - Hidden Investment pools?

- Can the Median Household Income pay for the fraudulent debts created by the CADs and the School Districts?

- Is there enforcement of laws including audits on the school districts? We have the responses from AG, Comptroller, State Auditor, TDLR, and TALCB stating they do not have enforcement authority.

- Where is the proof that the demand for the bonds, per line item, is paid for by the bonds?

- No payoff of bonds. Roll up and roll out.

- Where did the money go?

- The State’s matching funds is defrauding the federal government as a result of the “off” balance sheet contracts.

- No person voted with the 313 agreements

- The 313 agreements (pet projects) provide lucrative tax abatements and provide private industry incentives (advantages) that no taxpaying individual has.

- Taxpayers do not have a vote in the process.

- The districts have failed to deliver information requested in writing regarding the proposed or projected tax revenue(s) or the benefits from any of this “off balance sheet financing” methods.

- The legal counsel and consultants that negotiated the 313 contracts for the district were paid for by the solar farm owner/operators. This is a direct conflict of interest.

- The district failed to negotiate the best possible financial benefit to the district and therefore relieved the solar farm owner/operators of their fair share of local tax revenue from ad-valorem taxation on real property.

- The district failed to take advantage of the knowledge and experience of a taxpayer that would have resulted in a much favorable financial benefit for the district for many years.

- The district as of this date has not released information to taxpayers that has been requested by formal written request.

- Ad-valorem taxes are applied to Real Property based on the assessed values determined by, for example, the Hill County Appraisal District (HCAD). The district, working in unison with officials with HCAD, have demonstrated and levied ad-valorem taxes unequal and out of uniformity with the Universal Standards of Professional Appraisal Practice (USPAP) as required by law.

- School district officials have demonstrated further bias and prejudice against citizens and taxpayers not involved or part of a Chapter 313 Agreement by allowing solar farm owner/operators to use depreciation schedules for solar farm equipment installed on leased land acquired under the Chapter 313 Agreements. This allows solar farm owner/operators to benefit from both the lower taxable valuation stated in the contract but also by applying depreciating schedules to the solar farm equipment.

- School officials do not offer or extend the same tax relief opportunities as granted to solar farm owner/operators to the typical resident and property owner. Chapter 313 Agreements executed by district officials violate key tenants to the uniform and equal requirements as stated in USPAP.

- Depreciation schedules are not allowed as a means to reduce the taxable liabilities for the typical property owner, but instead typical homeowners are challenged annually with ever increasing property values and escalation of property taxes.

- School officials that have executed Chapter 313 Agreements to relieve solar farm owner/operators of their fair share of tax burdens are ear-marking projected increases in tax revenues as part of future bond referendums being pursued by school officials.

- These projected tax revenues are not guaranteed funds. There are no surety, or performance, bonds issued to guarantee future tax revenues will be realized for future years. The citizens and taxpayers had no voice or input into the decisions made by school officials. School officials did not have written approval from taxpayers for the decisions made by school officials and board members. This is Bond Election Fraud.

- If school officials maximized the available local tax revenues from ad-valorem taxes on Real Property, school districts would not need to issue bond referendums at all and could fund school districts from local resources and eliminate need for state of federal matching funds.

- School districts have demonstrated incompetence and gross negligence and understanding regarding how to maximize the available tax revenues that should be flowing into the local school district(s). This has resulted in further negative financial impact to local taxpayers and homeowners.

- School district officials have obligated taxpayers within the taxing jurisdiction of their respective district for a financial contract and agreement for ten years without taxpayer approval or vote. Tax abatements are a contract with a monetary value that guarantees or relieves a solar farm owner/operator financially for ten years. This contract can is used by solar farm owner/operators as collateral for loans used to construct solar farm projects.

- Chapter 313 Agreements that have been executed by school districts have become a negative line item in the annual budget. School board members have limited the bonding capacity of districts by obligating the district and taxpayers financially for years. These contracts are binding at this time unless the court(s) rule the agreements are illegal and violate the rights of citizens by eliminating them completely from the process.

- Texas Bond Program is insolvent.

- Your pockets are being picked while you sleep. Your equity from your amortization schedule is being stolen by the CADs fraudulent real estate tax, then bonds are created which can’t be paid off = 2 layers of theft on the back of all property owners. Further you don’t have that money to invest, stripping you of your future. (EQUITY STRIPPING)

- Tax Assessor Collector mails property tax bills that are fraudulent.

- Where is the Bond Schedule stating all outstanding individual bonds, including term, interest rate, underwriter, purpose, conditions, and their corresponding CUSIP numbers, and amortization schedules, from 9/1/2001 to 9/1/2025?

- Where is the amount of cumulative interest, outstanding interest and or compound cumulative interest on the outstanding bonds as of 9/1/2025?

- Where is the amount of interest to be paid in the future on the outstanding bonds starting 9/1/2025 to 9/1/2045?

- Where is the name of the Auditor and Auditing / Accounting Company, address, phone number and email address, hired by the School District.

- Databases at the CADs are compound fraud.

- They can’t confirm they are NOT breaking the law (they being the Attorney General, State Auditor, State Comptroller).

- Why is there a denial of the information?? Because they are complicit in aiding and abetting a criminal conspiracy to defraud?

- How do you know that the bonds can be paid off? Show us. CUSIPS – Median HH Income. How do you know the CUSIPS are being used when the Texas AG, State Auditor, State Comptroller, BRB, Texas Education Agency, Superintendents, and chief appraisers don’t have or won’t turn them over.

- The entities and individuals claim sovereign immunity to protect them from the fraud they committed.

- The SEC should immediately prohibit the State of Texas from gaining access to the bond market as the State of Texas Bond program is insolvent. – READ the Amicus.

- What proof exists that the certified tax rolls are correct?

- What proof exists that on an individual or global basis, the certified taxes are correct?

- If not correct and used as a basis for a property tax and school district bonds, how do homeowners recover from that lack of authority?

- Where is your verified data – DCAD, JCAD, HCAD, MCAD and all CADs in the State of Texas and across the U.S.?

- What evidence exists that the ARB panels utilize USPAP, to determine their Values?

- What method and under what laws do the ARB panels use to determine their values?

- The ARB under the Patel case written by the Supreme Court of Texas, cannot be the final determiner of value as the ARB does not have the authority under law to determine fraud.

- No one has met the requirement of proof.

- Where is the verification of evidence?

- Where is the verification that the process, as required in law, was adhered to?

- ARB – we can’t question the process by which the ARB comes to a number.

- Billions of dollars of fraudulent liabilities have been put on the property owner of which they are not required to pay.

- Willing suspension of disbelief.

- Nothing meets the standard of what is required. – that is the big con!

- What if mortgage rates go up?

- What if the property values go down by 10, 20, 30% with regard to the CAD’s bond fraud? Where is the Probability of Default analysis?

- Bonds have derivatives allegedly to protect the values. What is the probability of the derivatives paying off when the system implodes due to fraud?

THE DIFFERENCE OF SURVIVING OR BANKRUPTCY IS THE REAL ESTAE TAX.