We Don't Need Arguments. We Have Facts, Law & Math.

DCAD and SPENCER have FRAUD!

By Mitchell Vexler, March 13, 2026

Also see the video titled, Something PIVOTAL Just Happened with PROPERTY TAX.

https://www.youtube.com/watch?v=PgAEHnlVFwA

Per the court’s request, opposing counsel was asked to respond to the petitioners’ request for re-hearing. In his response, the opposing counsel, who as an officer of the court is attempting to mislead and lie to the SCOTX, as the truth is that opposing counsel is not just acting as defense for SPENCER or DCAD but is in fact aiding and abetting a criminal conspiracy to defraud as a participant in the scheme to settle cases in which there is no basis in law, fact or math to begin with. Opposing counsel is paid on an annual basis to be the fixer for DCAD and intends to keep the gravy train of taxpayer funds rolling into their coffers. Opposing counsel has zero credibility as does DCAD and SPENCER.

Opposing counsel has shown their road map within their Response, being the same pattern and practice to defraud not only across Texas but across the U.S. Here and now, is a portion of the irrefutable evidence that opposing counsel does not want to discuss or allow the presentation of in front of the SCOTX or any court.

Due to intentional delay, this case has been 3 years in the making and now there are the 2024 and 2025 Vexler cases on its heels. The evidence grows as does the fraud being perpetrated upon the Citizens of Texas. These cases should not be bifurcated but upon remand to the lower court immediately consolidated. All the evidence is available for the world to see at www.mockingbirdproperties.com/dcad and nothing is going to change the evidence of the crimes that have been committed.

Opposing counsel intends to lead and mislead the courts including the SCOTX away from the evidence because there is no defense for the crimes committed as it is the testimony under oath of multiple individuals from within DCAD that is traced right to the documents submitted to the SCOTX.

How can the administrative process, under Administrative Law, lead to fraud?

Ultra Vires is a due process violation. (A) Ultra Vires are acts committed beyond legal power or authority, meaning the frauds perpetrated by DCAD and SPENCER upon the Citizens of Denton County.

An Ultra Vires action is outside of Administrative Law. (B)

If fraud can occur under due process (as stated and claimed by opposing counsel) then that must be a due process violation. (C)

The net result is a State “taking” without due process which is mass fraud upon society by ignoring both Ultra Vires and Administrative Law. (D)

If A = B and B = C, which also = D, then A = D

The statute cannot be defended, and neither can the actions of DCAD or SPENCER or opposing counsel because the result is fraud.

The Appraisal process cannot be immune from scrutiny.

See The Importance of the Vexler Case to Texas & the United States as there is a high probability that these crimes are being committed wherever School Districts raise bonds.

In short, and as a response to the opposing counsel’s further attempted misleading statements upon the SCOTX and the Citizens of Denton County and Citizens of Texas, I hereby offer a very short list of irrefutable facts from which there is literally no defense for SPENCER or DCAD or opposing counsel.

In the October 12, 2023 DCAD Board Meeting, the Deputy Chief Appraisers (Littrell & Ashlock) and the Chief Appraiser (Spencer) discuss their manipulation(s) of data within the software, and the removable of data to change it and then reload it to the software program. Notice the words, "workarounds” and “manipulate”.

- October 12, 2023 meeting audio recording, located in our audio recording archive

- October 12, 2023 partial transcript of audio recording

Where exactly is the word “workaround” in USPAP, Uniform and Equal, in American Procedures Act and Texas Procedures Act and within any document connected to any CAD in the U.S.? Tampering with government documents is illegal under various laws, including 18 U.S.C. § 641, which prohibits the theft or alteration of government property, and 18 U.S.C. § 1519, which addresses the destruction or falsification of records in federal investigations. Violating these laws can result in severe penalties, including fines and imprisonment.

Now also consider the February 15, 2024 DCAD Board Meeting; listen to audio file saved in the audio recording archive or read the partial transcript of this meeting. The DCAD Board congratulates the Chief Appraiser and his staff, saying, “they are truly masters at guessing.”

Where exactly is the word “guessing” in USPAP, Uniform and Equal, in APA and Texas Procedures Act and within any document connected to any CAD in the U.S.?

Texas Penal Code - PENAL § 37.10. Tampering with Governmental Record

(as of January 01, 2024)

(a) A person commits an offense if he:

(1) knowingly makes a false entry in, or false alteration of, a governmental record;

(DON SPENCER FALSIFIED THE TAX ROLL along with HOPE MCCLURE per the evidenced complaint filed with the Texas State Comptroller – DCAD employees falsify property records and values rendering the databases 100% irretrievably fraudulent)

(2) makes, presents, or uses any record, document, or thing with knowledge of its falsity and with intent that it be taken as a genuine governmental record;

(3) intentionally destroys, conceals, removes, or otherwise impairs the verity, legibility, or availability of a governmental record;

(4) makes, presents, or uses a governmental record with knowledge of its falsity; or

(5) possesses, sells, or offers to sell a governmental record or a blank governmental record form with knowledge that it was obtained unlawfully.

A synonym for “workaround” is fraud!

There are over 1,100 exhibits at www.mockingbirdproperties.com/dcad including depositions, audio and DCAD’s own documents, DCAD’s databases, DCAD’s computer entry logs, all of which prove the pattern and practice to defraud.

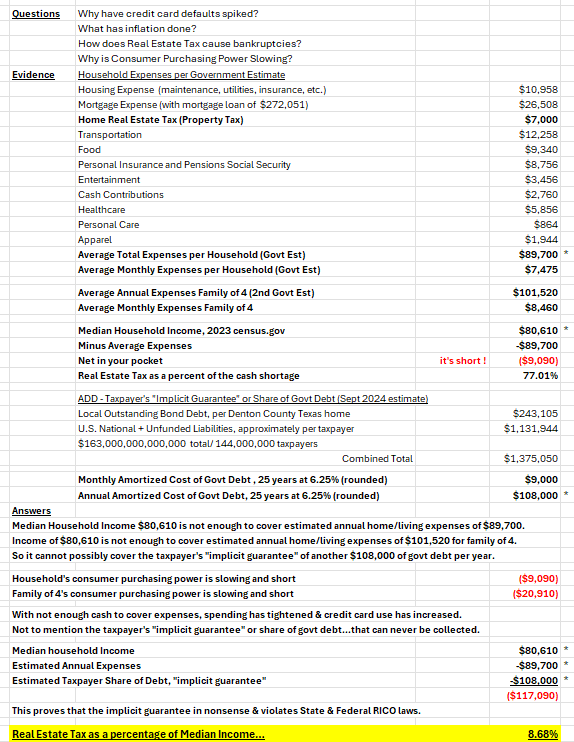

The economic damages to the Denton County Property Taxpayers are in the Billions of Dollars, dollars that have been stolen from the property owners, forcing considerable inflation that would not exist but for the fraud. Remember this is happening across the U.S.

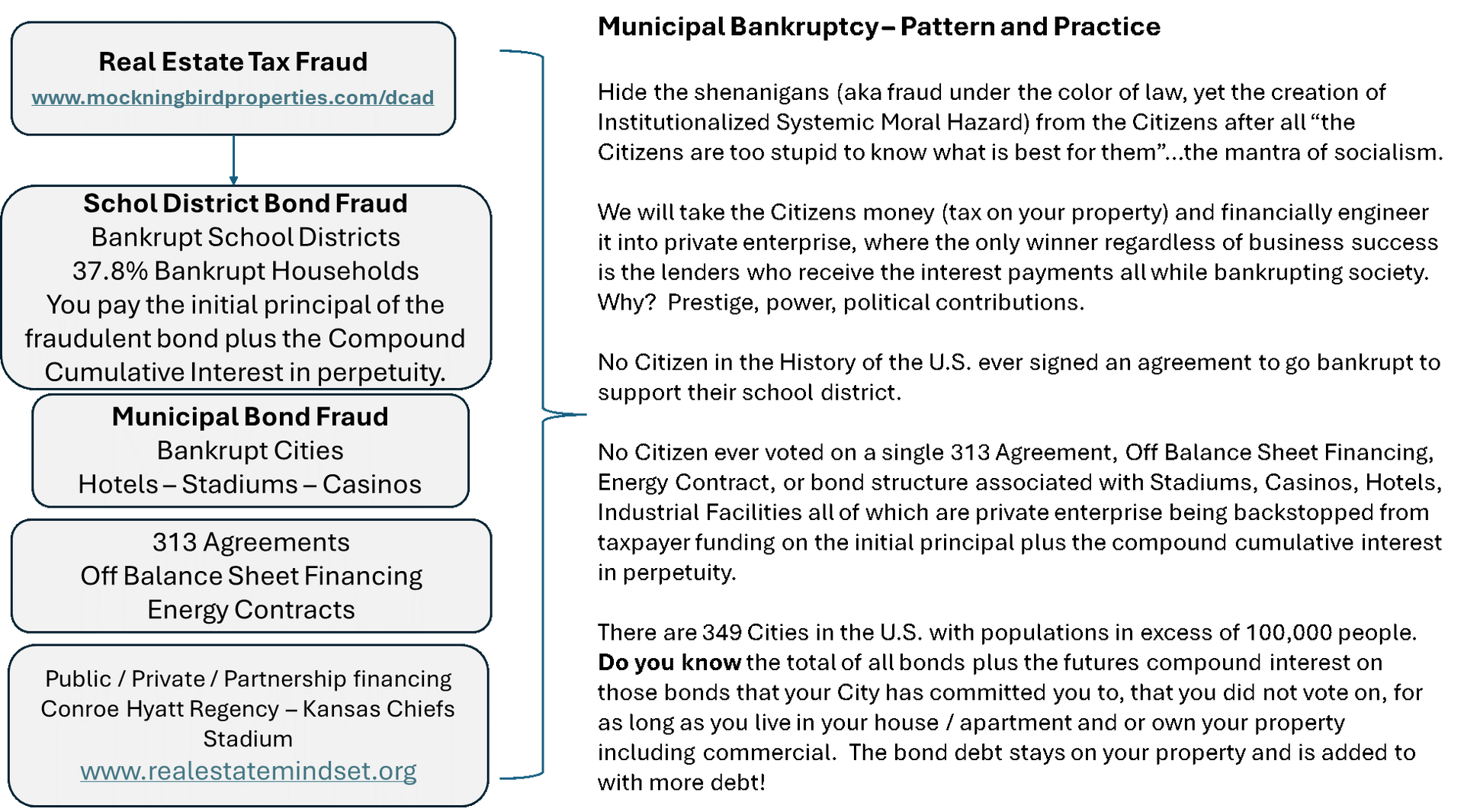

DCAD and SPENCER are fraudulently increasing property values (with the knowledge of opposing counsel) to allow the School Districts, via pre-determined budgets, that raise bonds and who are committing bond fraud and accounting fraud against all real estate owners, property tax payers, bond holders as well as 401K and Pension holders, all in violation of Constitutional Rights of the victims, being SOCIETY at large. The pre-determined budgets are presented at meetings between the CAD and the School Districts, and the result is Cooking the Books.

The Median Household Income does not exist to pay for the interest on the fraudulent bonds outstanding never mind paying down or paying off the bonds. The interest is compound cumulative on top of the fraudulent bonds, and the school districts do not pay off the bonds, in favor of rolling them out in time and rolling the interest rate up. Then the school districts raise more bonds which creates more debt on top of the current fraudulent bonds. This is a Ponzi scheme. As the property values are fraudulent, so must be, the bonds.

DCAD and SPENCER are guilty of:

- Creating fake income and expense data,

- Destroying Appraisal Work Records, before and after subpoena,

- Hiding property values from the Public,

- Utilizing multiple disconnected databases with different data between them,

- Manipulating the property valuations in Excel outside of the already corrupted databases, and then further increasing values at the demand of the State Comptroller via the Property Valuation Study,

- Deploying fraudulent and inconsistent subcategories / Class Codes for the sole purpose of manipulating values in their sole discretion outside the confines of USPAP, Mass Appraisal Standards, and the Texas Property Tax Code, and with no uniformity of application of the law and no adherence to the law. The Software at the CADs is design to allow the employees to cheat, and if that is not good enough for them, the employees have “workarounds”,

- Intentionally not using legitimate comparisons,

- Aligning and increasing Appraisal Notice Values, made up to suit pre-determined budgets which have absolutely nothing to do with USPAP or quantifying the true market value of properties,

- The CADs are depending on the ARB process to buttress the crimes committed thus making the ARB members co-conspirators in the CADs crime of fraud,

- ARB members are not independent as required in law, and are unqualified in all respects to property valuation, math, USPAP, and appraisal law,

- Creating “workarounds” of the software including taking 60,000 properties out of the data base, manipulating them in excel and putting them back rendering the entire data base 100% a fraud. Data Set A, B, C, D, E. If B is wrong, then so is A, and then it compounds the fraud annually. In the last 5 years property values according to the CAD went up by 100%, yet inflation according to the Federal Reserve has only gone up 15%. Meaning 85% of the property rise in value is fraudulent. Just to get a value where we were 5 years ago means a minimum reduction of 40% of the current fraudulently assessed value.

- Violating USPAP, Mass Appraisal Standards, TDLR, TALCB, Texas Property Code, Texas Constitution, The Constitution of the United States of America, IAAO, TAAO, Appraisal Foundation, Appraisal Institute, and a host of both state and federal law which is seen in the Violations Reviewed.pdf which is on the website mockingbirdproperties.com/dcad,

- Violating Texas Penal Code - PENAL § 37.10 (See Violations.PDF),

- Nothing meets the standard of what is required – That is the BIG CON and the FRAUD being perpetrated upon the property owners of Denton County and throughout Texas.

- The evidence is irrefutable, insurmountable and there is no defense.

DCAD and SPENCER are guilty of defrauding the public. This case must be remanded to be adjudicated on the merits of fraud so that all the evidence is entered on record and Mr. Spencer forced to testify.

Not only does Vexler have this 2023 case but now has the 2024 and 2025 cases. This evidence is not going away and in fact continues to grow as does the compound cumulative interest on the fraudulent principal of the bonds.

See Preamble to Whitewashing of Your Tax Dollars, Pattern and Practice.

In another reference to opposing council attempting to mislead the SCOTX by stating that Vexler offers nothing new here is more proof of opposing council’s misleading statements.

This is the Criminal Complaint (link) that was filed with the DOJ, FBI and SEC. As a result of this Criminal Complaint, Texas AG Paxton ordered a 1,000 district investigation on December 7, 2025 (link), into the overvaluation and he did so on his way out of the AG office to run for Senate. Read who the complaint is about and how the crimes were committed.

There are independent reports both before and after the 2023 Vexler case that also prove the intent to defraud and the methods used. Here are some examples:

- The California Policy Center Report details the methods of bond election fraud and they knew back in 2015 the bonds were toxic. Now they are toxic, raised to the power of The Rule of 72, plus cumulative bond fraud.

- In the Johnson County Appraisal District (JCAD) report dated February 7, 2026, examine page 4. Notice the word “workaround”! The same “workaround” as stated by Deputy Chief Littrell of the Denton CAD in 2023 except this JCAD report is current.

- Review the Kansas Special Committee on Taxation Report, Residential Appraisal Testimony, dated September 18, 2025.

- In March 2024 Professional Consulting Services of the International Association of Assessing Officers (PCSIAAO) issued a Gap Analysis Report on their review of the Denton Central Appraisal District (DCAD). The resulting report is actually an admission of guilt on/by DCAD on their property tax appraisal practice failures. This is the short version and analysis of the report, summary notes of report.

When examined together including DCAD’s own Gap Analysis Report, the evidence of systemic fraud is laid bare for the world to see.

Opposing counsel wants nothing more than to bury this entire case, but that will not happen.

To make sure this case and the frauds related thereto are not buried, and are heard both by the Courts and in the Court of Public Opinion, the Mockingbird Properties DCAD website section, https://www.mockingbirdproperties.com/dcad, exists, along with every stitch of documentation including but not limited to the above referenced independent reports that we have, plus the Articles, Letters, and Discussions, all of which is for the benefit of all Citizens, in Texas and across the U.S., and any country that claims to utilize USPAP.

The evidence is the evidence from which there is no defense. USPAP is not being adhered, rendering the Appraisal Foundation and USPAP completely meaningless in favor of fraud.

Why Should the Supreme Court of Texas Care:

- If ARBs are the exclusive forum, then property owners have no meaningful remedy for fraud. That is exactly the type of constitutional anomaly the Supreme Court of Texas exists to resolve.

- The Patel case is the Supreme Court of Texas own precedent. Extending it to property taxation would be a doctrinal development of Texas constitutional law, which justifies granting review.

- The Supreme Court of Texas is the ultimate guardian of the state’s uniformity mandate, and systemic non-uniformity across counties is squarely within its constitutional oversight role.

- Expands the boundary of takings jurisprudence into the property-tax context—again, a constitutional development.

- Goes directly to the Court’s institutional role as the guarantor of judicial access.

- This is not just Denton County—it’s systemic and affects billions in state-backed school district bonds. That’s exactly the kind of statewide crisis the Supreme Court of Texas exists to address.

Bottom Line

The Supreme Court of Texas has, in the last five years, reviewed multiple CAD cases involving equal-and-uniform taxation and jurisdictional barriers to court review. Vexler’s filed petition fits directly into those doctrinal tracks — but raises them on a broader constitutional and statewide scale.

Why This Matters

SCOTX does review appraisal district valuation disputes—especially when statewide tax policy or judicial review procedures are implicated.

Not only are the procedures implicated, so are the individuals, who in totality, are responsible for billions of dollars of theft and opposing counsel shares in this liability. How many times has opposing counsel lied in settlement discussions claiming a cap on legal fees, claiming the accuracy of DCAD, hiding evidence, and negotiating settlements that have no basis in math, law or fact, just for the sake of settling the case? The effect of opposing counsel as the “fixer” for DCAD, hiding behind sovereign immunity and negating Ultra Vires, is the continuation of the fraud upon victims who don’t understand the depth and pervasiveness of the fraud.

The constitutional questions posed within the Vexler case are equal and uniform taxation, open courts, due course of law, and the limits of administrative exclusivity, all of which singularly or together are natural extensions of the Court’s existing precedent.

Conclusion of Authorities

These authorities confirm that Petitioners’ claims lie within categories of disputes the Supreme Court of Texas has repeatedly reviewed. Far from being routine tax complaints, the issues here implicate fundamental constitutional protections, jurisdictional access to the courts, and the financial integrity of the state’s tax and bond systems. Review is therefore both appropriate and necessary.

Jurisdictional Statement

This case presents questions of exceptional constitutional and statewide importance. The Court of Appeals’ decision insulates systemic fraud in property appraisals from any judicial remedy by confining taxpayers to appraisal boards that lack authority to adjudicate fraud. That result violates the Open Courts guarantee (Tex. Const. art. I, § 13) and Due Course of Law protections (art. I, § 19), as recognized in Patel v. TDLR. It also undermines the mandate of Equal and Uniform Taxation (art. VIII, § 1(b)) and strips equity in violation of the Takings Clause (art. I, § 17). Because these appraisal practices directly underpin billions of dollars in Permanent School Fund–guaranteed bonds, the case implicates not only constitutional rights of Texans but also the financial stability of the State. Review is therefore proper under Tex. Gov’t Code § 22.001(a)(2) and (6).

Again, I have stated in writing, and on video many times, either the law exists, or it doesn’t.

No Constitutional Entity can allow fraud to escape.

Here is the most important question for opposing counsel representing the CAD, its employees, and counsel itself, as an officer of the court:

If you don’t intend to allow the resolution and discovery by every Texan regarding property tax fraud and related school district bond fraud being committed upon them, why is that?

Note to the Citizens of Texas and throughout the Unites States:

The attorneys who are co-conspirators of the CADs play every trick in the book including delaying hearings, withholding evidence, destroying evidence, and wrangling settlements not based on math, fact or law, all in an attempt to wear down their victims. This is why I have said that it makes sense to join forces without multiple property owners and if feasible in your State, file class Action lawsuits. Given the evidence outlined in this video and in this document, and the map of criminality submitted by opposing counsel to the SCOTX, which every legitimate attorney in the U.S. should study, and given the pattern and practice of the CADs and School Districts to defraud, as documented onwww.mockingbirdproperties.com/dcad, every property owner should be looking to file suit, and jam the court system with class action suits, criminal complaints, and law suits against every participant who dares participate in the equity stripping of your property and your retirement.

Every property owner and every Citizen now have the CADs and School Districts play book, courtesy of opposing counsel, and you now also have the response and evidence that proves their playbook is a fraud, just like they are.

In 1775 “NO taxation without representation” was the battle cry via the War of Independence and is just as important and potent today as a result of the fraud being committed upon Society.

Opposing counsel’s response is asking the SCOTX to guarantee taxation without representation. Under no circumstances is that acceptable.

We have the documented history of bond election fraud by the School Districts, bond fraud, accounting fraud, overvaluation and over taxation fraud by the CADs. There are gigabytes of evidence are at www.mockingbirdproperties.com/dcad which can be short listed to:

- No homeowner or renter voted to have 8.6% of their gross income paid in property taxes.

- No homeowner or renter agreed to bond election fraud.

- No homeowner or renter agreed to school district bond fraud, which cannot be paid off.

- No homeowner or renter agreed to be the guarantor for bond fraud by the School District or the fraud of overvaluation and over taxation by the CADs and the criminals therein.

- No homeowner agreed to lose the roof over their head or go bankrupt due to tax lien foreclosure.

- No commercial property owner agreed to allow false income and expense statements to be created by individuals within any CAD from which money is extorted.

- No homeowner agreed to a ground lease which is the net effect of the overvaluation and over taxation along with the equity stripping of what would be their amortized debt reduction of their mortgage.

Clearly, under the current fraud, we are back to “Taxation Without Representation”. However, this is far worse because the taxation that is funding fraudulent school district bonds and accounting fraud today will continue for the next 20 to 40 years, as it is a compound cumulative debt, which can never be paid off.

Are we now at the crossroads of civil war based on taxation without representation as was seen in 1775, or do we bypass the civil war and go to 1778, wherein Parliament finally passed the Taxation of Colonies Act which repealed the taxes, and hope that it is not too late?

As is recorded in history, governments can’t see the forest through the trees, and here in the United States, we have a tendency to walk to the very edge of the cliff and peer into the abyss before backing up to safer ground. Perhaps it might be an excellent idea to remand the Vexler case to the lower courts to be adjudicated on its merits, being that of fraud, wherein the ultimate conclusion, in order to prohibit the bankruptcy of millions of Citizens, will be the repeal of all property tax in favor of the Uniform States Sales Tax.